Companies use contingent capital facilities to supplement existing capital resources, improve funding diversification and enhance financial flexibility through immediate access to committed capital. Contingent capital can take many forms, with revolving credit facilities being one obvious example. A less well-known capital markets contingent capital product, pre-capitalized trust securities (“P-Caps”), have some features similar to those of a revolving credit facility, but can be much longer dated with less counterparty risk. In this article, we provide a brief introduction to P-Caps, including the potential benefits and considerations.

The P-Caps Structure

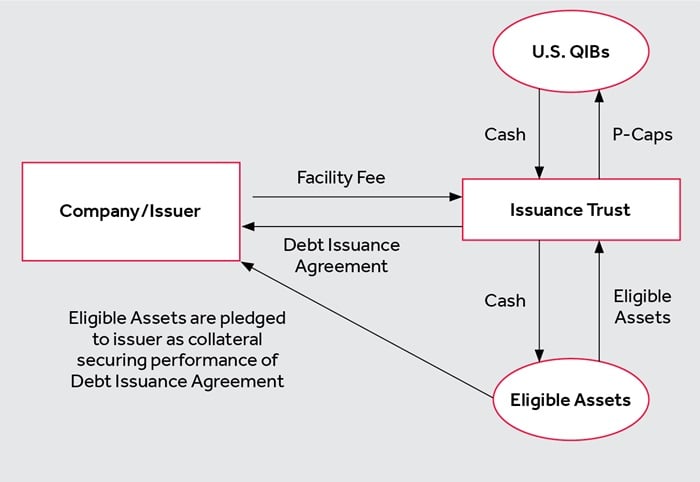

Generally, in a P-Caps transaction, the company creates a new Delaware statutory trust. That trust issues trust securities to qualified institutional buyers in a Rule 144A offering. The proceeds from the issuance are invested by the trust in a portfolio of principal and interest strips of U.S. Treasury securities (“Eligible Assets”) that, together with the facility fee described below, matches the expected payments on the trust securities. The basic structure is depicted below:

Concurrently with the issuance of the trust securities, the trust enters into a facility agreement with the company. The facility agreement provides the company with an issuance right (the “Company Issuance Right”) that permits the company, at its option, to issue senior notes to the trust and require the trust to purchase such senior notes with an equivalent amount of the Eligible Assets. The company is required to exercise the Company Issuance Right in full upon certain automatic or mandatory triggers, including events of bankruptcy, certain payment defaults, or if the company’s consolidated net worth falls below a threshold amount. In return for the Company Issuance Right, the company pays the trust a facility fee. The facility fee together with the income from the Eligible Assets is equal to the coupon on the trust securities.

The trust securities are typically rated in line with the company’s senior notes rating and are designed to mimic an investment in those notes, providing investors a risk profile equivalent to a direct investment in the company’s senior debt.

If the company wants to exercise the Company Issuance Right and receive the Eligible Assets, it delivers a notice to the trust. Assuming a full exercise of the Company Issuance Right, the trust’s sole assets will be the company’s senior notes. Most P-Caps facilities permit the company to exercise the Company Issuance Right in part, in which case the company would issue a portion of the contractually agreed maximum aggregate amount of senior notes to the trust and receive the equivalent amount of Eligible Assets. The trust’s assets would then comprise the remaining Eligible Asset and the senior notes that were issued. The facility fee on the unissued senior notes, the coupon on the senior notes and the income from the remaining Eligible Assets would provide sufficient funds to pay the coupon on the trust securities.

Structuring Options

The basic P-Caps structure described above can be modified to provide the company with additional flexibility and optionality. Structuring options in existing P-Caps facilities have included the following features:

- Refreshability. Recent P-Caps structures have allowed the company to draw on the facility, repay the facility and then re-borrow as frequently as it would like during the life of the facility. This is made possible by the inclusion of a repurchase right that allows the company to repurchase any or all of the senior notes then held by the trust, in exchange for Eligible Assets that the company holds or purchases in the market.

- Assignability. Another modification allows the company to direct the trust to grant the Company Issuance Right to one or more assignees of the company, typically direct or indirect subsidiaries of the company. Upon exercise of the Company Issuance Right, the company would issue its senior notes to the trust, but the trust would deliver the Eligible Assets to the assignee. This feature may be useful if there is a desire to move capital into a regulated subsidiary (e.g., a regulated insurance company or bank) in advance of a bankruptcy filing by an unregulated holding company.

- Pledge. In other P-Caps transactions, primarily in the non-insurance space, the Eligible Assets have been pledged to lenders to fully collateralize the company’s letter of credit facility. The pledge would be enforceable by the lenders, and the Company Issuance Right triggered, upon the occurrence of an event of default under the letter of credit agreement.

Benefits

There are several key benefits of P-Caps compared with other sources of capital:

- Leverage Neutral. Until the senior notes are issued to the trust, the P-Caps are not reflected on the company’s balance sheet and not included in the company’s financial leverage. The off-balance sheet nature of the P-Caps structure enables the company to proactively prepare for contingencies, while ensuring the company does not advertise an artificially inflated leverage level or breach any leverage-related financial covenants prior to issuance.

- Rating Positive. Rating agencies generally view P-Caps as a credit positive because they improve the company’s access to liquidity, especially in times of stress. In addition, the trust securities are typically rated in line with the company’s senior notes as investors are in effect investing in the senior credit of the company.

- Standby Credit. The immediate liquidity offered by P-Caps provides for a reliable source of financing during a stress event. P-Caps are a form of standby credit which is available prior to maturity regardless of market windows, broader economic conditions or issuer specific events. This is significant, as other avenues of capital may be unavailable or prohibitively expensive during a liquidity shortfall. For example, in contrast to a revolving credit facility, there is no counterparty risk when the company wants to draw on the facility because the Eligible Assets are on hand with the trust and the trust is contractually obligated to provide the Eligible Assets in exchange for the company’s senior notes.

- Tax. The company will receive a net tax deduction equivalent to the amount of the facility fee payable by the company to the trust while the facility is undrawn. The tax deduction offsets the facility fee, which helps reduce the overall cost of the P-Caps.

- Long-Dated. Issuances of P-Caps have been for 10, 20 and 30-year maturities. These are significantly longer maturities than the typical revolving credit facility.

- Covenant-Lite. The trust securities and the underlying senior notes have few, if any, covenants. To the extent that these facilities do include restrictive covenants, they typically mirror the covenants in the company’s other senior indebtedness.

- Use of Proceeds. If the contingent capital facility is drawn, the company receives the Eligible Assets, which are expected to be liquid securities, and does not have any restrictions on its use of the Eligible Assets. The Eligible Assets can be held as U.S. Treasury strips or converted into cash for immediate use.

Considerations

The benefits of the P-Caps should be weighed against the following considerations:

- Cost. The company is required to pay the facility fee even if the facility is undrawn, resulting in ongoing costs in excess of a typical revolving credit facility undrawn commitment fee. There are also additional transaction costs related to monetizing Eligible Assets when the Company Issuance Right is triggered and sourcing Eligible Assets to refresh the facility if it is drawn and repaid.

- Fixed Maturity. If the Company Issuance Right is exercised and the senior notes are issued to the trust, the senior notes will need to be repaid or refinanced at maturity which is fixed regardless of when the Company Issuance Right is exercised, subjecting the company to eventual refinancing risk based on market conditions.

- Credit Risk of Company. As noted above, the facility automatically or mandatorily triggers after the company goes into bankruptcy or defaults, or if the company’s net worth declines below a specified threshold. While this automatic issuance of senior notes would immediately increase the company’s liquidity, it also increases its outstanding indebtedness, which would be treated pari passu with the company’s other existing senior indebtedness.

- P-Cap Pricings. The coupon the company pays on the P-Caps is generally slightly higher than the interest rate paid on the company’s revolving credit facility, which reflects the structured nature of the product, the longer-dated maturity and the company’s typical senior notes pricing.

Final Thoughts

There have been a limited number of P-Caps transactions over the last 10 to 15 years and those transactions have been executed primarily by insurance companies. However, more recently, companies in the energy sector have taken advantage of the structure, and it is fair to say that the structure is industry agnostic. P-Caps are a reliable, pre-emptive tool a company can employ to prepare for unforeseen stress events, closed market windows, opportunistic M&A funding or other liquidity needs.

P-Caps can be an effective, supplemental source of liquidity and capital that provides a company with long-dated flexibility and for the right company is a great addition to the company’s capital structure. We would be happy to discuss the structure and the related costs and benefits with any interested issuer.