Key Takeaways:

- On March 6, 2024, the SEC adopted its long-awaited rule on the “Enhancement and Standardization of Climate-Related Disclosures for Investors.” Subject to applicable phase-in periods, virtually all SEC registrants, including companies conducting an initial public offering, will be subject to the requirements of the final rule. Notable exemptions include private companies that are parties to business combination transactions and Canadian registrants that utilize the Multijurisdictional Disclosure System.

- Registrants will be required to comply with enhanced qualitative disclosure requirements contained in a new subpart 1500 of Regulation S-K and additional financial statement disclosure requirements contained in a new Article 14 of Regulation S-X. A number of the disclosure requirements are subject to materiality-based qualifiers, including those related to GHG emissions, climate-related risks, board and management oversight of climate-related risk, transition plans and the use of scenario analyses and internal carbon prices.

- Since the SEC adopted the final rule, seven suits challenging the final rule have been filed. However, registrants do not have the benefit of waiting to see what the outcome of the pending litigation is as the SEC considers the transition periods to be lengthy and assumes registrants will be preparing to comply on the effective dates.

On March 6, 2024, the U.S. Securities and Exchange Commission (the “SEC”) adopted its long-awaited rule on the “Enhancement and Standardization of Climate-Related Disclosures for Investors” (the “Final Rule”). The Final Rule applies to nearly all SEC registrants, including foreign private issuers (“FPIs”), and is intended to facilitate the disclosure of “complete and decision-useful information about the impacts of climate-related risks on registrants” and to improve “the consistency, comparability, and reliability of climate-related information for investors.”

The Final Rule is available here and the accompanying fact sheet is available here.

In this companion to our March 8, 2024 and March 14, 2024 updates, we provide a detailed summary of key provisions of the Final Rule and our related analysis and insights.

General Observations

Regulations and Forms Amended

The Final Rule’s disclosure requirements are contained in new subpart 1500 of Regulation S-K, which primarily requires new qualitative disclosures, and new Article 14 of Regulation S-X, which requires new financial statement disclosures. Subject to a phase-in period, information must be disclosed in XBRL format, per Regulation S-T standards. The Final Rule amends several forms under the Securities Act of 1933, as amended (the “1933 Act”) and Securities Exchange Act of 1934, as amended (the “1934 Act”), including Form 10-K (for domestic registrants) and 20-F (for FPIs).

Debevoise Insight

Subject to applicable phase-in periods, virtually all SEC registrants, including companies conducting an initial public offering, will be subject to the requirements of the Final Rule. Notable exemptions include private companies that are parties to business combination transactions and Canadian registrants that utilize the Multijurisdictional Disclosure System.

Materiality

In response to concerns expressed by commenters that the proposed rule (the “Proposed Rule”) would create significant compliance costs and require immaterial and voluminous disclosure, the Final Rule added materiality-based qualifiers to a number of the disclosure requirements, including those relating to greenhouse gas (“GHG”) emissions, climate-related risks, transition plans and the use of scenario analyses and internal carbon prices.

In those instances where the Final Rule references materiality, consistent with existing disclosure rules and market practices, registrants should rely on traditional notions of materiality: information is material “if there is a substantial likelihood that a reasonable investor would consider it important when determining whether to buy or sell securities or how to vote or such reasonable investor would view omission of the disclosure as having significantly altered the total mix of information available.” As in other cases, materiality determinations that registrants make under the Final Rule will be fact-specific and incorporate both quantitative and qualitative considerations. Materiality decisions in the context of climate-related disclosure are likely to be particularly complex, as there is no existing framework by which to consider materiality of climate-related matters, such as GHG emissions. Registrants may need to consider certain aspects of the Final Rule in making materiality determinations, such as the quantitative disclosure thresholds under Regulation S-X, and may also need to consider disclosure they have made pursuant to other emissions reporting regimes (such as the European Union’s Corporate Sustainability Reporting Directive (“CSRD”)) or disclosure they have made on a voluntary basis. Additionally, the Final Rule uses both “materially impacted” and “reasonably likely to materially impact” as qualifiers for many disclosure requirements, thereby requiring registrants to undertake a prospective analysis similar to the discussion of material events and uncertainties contained in the Management Discussion and Analysis (“MD&A”).

The SEC offers some guidance to issuers in the adopting release. For example, in the context of Item 1502 of Regulation S-K (actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model and outlook), the SEC enumerates types of material impacts that a registrant should consider. These include impacts on (i) business operations, including the types and locations of its operations; (ii) products or services; (iii) suppliers, purchasers or counterparties to material contracts; (iv) activities to mitigate or adapt to climate-related risks; and (v) expenditures for research and development.

The adopting release also reveals the interrelated nature of materiality assessments in the context of climate-related disclosures. For example, the SEC notes that a registrant’s GHG emissions could be material if their calculation and disclosure are necessary to allow investors to understand whether those emissions subject the registrant to a transition risk that has materially impacted or is reasonably likely to materially impact its business, results of operations or financial condition, or to enable investors to assess targets, goals or transition plans. The SEC provides the following example:

“…where a registrant faces a material transition risk that has manifested as a result of a requirement to report its GHG emissions metrics under foreign or state law because such emissions are currently or are reasonably likely to be subject to additional regulatory burdens through increased taxes or financial penalties, the registrant should consider whether such emissions metrics are material under the final rules. A registrant’s GHG emissions may also be material if their calculation and disclosure are necessary to enable investors to understand whether the registrant has made progress toward achieving a target or goal or a transition plan that the registrant is required to disclose under the final rules.”

The SEC acknowledged this complexity, and made clear their expectation that issuers develop systems and processes to assess materiality, in stating that registrants could incur significant costs to assess and monitor the materiality of their emissions, even in situations in which they ultimately determine that they do not need to provide disclosure.

Debevoise Insight

In addition to issuing comment letters addressing specific disclosure requirements under the Final Rule, we anticipate that the SEC will continue issuing comment letters asking registrants to explain how the materiality determinations that informed climate-related disclosures (or lack thereof) were made, as the SEC has done since issuing its “Commission Guidance Regarding Disclosure Related to Climate Change” in 2010 (the “2010 Guidance”). Registrants that have made public statements regarding the materiality of their climate-related risks and GHG emissions should carefully consider those statements in assessing their approach to disclosures pursuant to the Final Rule. We note that the SEC has consistently rejected conclusory statements regarding materiality, instead requiring registrants to provide the SEC with detailed analysis regarding how materiality determinations were made.

Further, registrants will need to assess whether appropriate disclosure controls and procedures are in place to ensure that the information required to make the relevant materiality determinations is available to management and that adequate processes are in place to record those determinations, even if a registrant ultimately determines that it does not need to provide disclosure.

Business Combination Transactions

The Final Rule does not apply to private companies that are parties to business combination transactions (as defined by Rule 165(f) of the 1933 Act) involving a securities offering registered on Form S-4 or Form F-4 and certain business combination transactions for which a proxy statement on Schedule 14A or an information statement on Schedule 14C is required to be filed.

Debevoise Insight

Absent further guidance from the SEC, a registrant will need to comply with the applicable reporting requirements with respect to a business or asset acquired at any time during a fiscal year, including with respect to acquisitions that close as late as the fourth quarter of a fiscal year.

Key Provisions of the Final Rule

Financial Statement Metrics (Regulation S-X Amendments)

The Final Rule amends Regulation S-X to require registrants to disclose information on the impact of climate-related risks (both physical and transition) on the registrants’ business in their consolidated financial statements. Specifically, the Final Rule requires disclosures about the following categories:

- Expenditure and capitalized cost metrics; and

- Financial estimates and assumptions materially impacted by climate-related events and transition plans disclosed by the registrant.

The Regulation S-X disclosures also must include contextual information regarding how metrics are derived, including descriptions of significant inputs and assumptions, significant judgments made, other information important to understand the impact on financial statements and, if applicable, any policy decisions adopted by the registrant in the calculation of the metrics.

Consistent with other changes made throughout the Final Rule, the SEC declined to adopt the proposal explicitly allowing, but not mandating, disclosure of the impact of any climate-related opportunities on any of the financial statement metrics disclosed pursuant to this section.

Basis of Calculation, Accounting Principles and Historical Periods

The Final Rule requires a registrant to (i) calculate the financial statement disclosure using financial information that is consistent with the scope of the rest of the registrant’s consolidated financial statements (including its consolidated subsidiaries) and (ii) apply the same accounting principles it is required to use for the rest of its consolidated financial statements. Disclosure must be provided for the registrant’s most recently completed fiscal year and, only to the extent previously disclosed or required to be disclosed, for the historical fiscal year(s) included in the consolidated financial statements in its filing.

Scope of Disclosure

In a significant change from the Proposed Rule, the Final Rule does not require registrants to provide disclosure on a line-by-line basis or to provide quantitative disclosure related to any efforts to reduce GHG emissions or otherwise mitigate exposure to transition risks. Instead, registrants are required to disclose the aggregate amount of (i) expenditures expensed and (ii) capitalized costs incurred as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures and sea level rise. In addition, registrants are required to disclose where such aggregate expenditures are presented on the income statement or balance sheet.

Debevoise Insight

The Final Rule requires registrants to determine what constitutes a “severe weather event” or a “natural condition.” The SEC noted in the adopting release that “registrants will have the flexibility to determine what constitutes a severe weather event or other natural condition based on the particular risks faced by the registrant, taking into consideration the registrant’s geographic location, historical experiences and the financial impact of the event on the registrant, among other factors."

Commissioner Hester Pierce in her Commissioner Statement raised a number of questions with regard to the term “natural condition,” including what a severe natural condition is and whether a global health pandemic would be a severe natural condition. The latter question went unresolved, highlighting inherent ambiguity in the definition, though Chief Accountant Paul Munter suggested that a natural condition could ordinarily be understood to be a consequence of a physical risk.

In addition, the Final Rule requires registrants to attribute a cost, expenditure, charge, loss or recovery to a severe weather event or other natural condition when the event or condition is a “significant contributing factor” in incurring the cost, expenditure, charge, loss or recovery.

It will be important for registrants to have in place policies and processes to make the determinations required under Article 14-02 of Regulation S-X in order to ensure consistency and reliability. Such policies and processes must form a part of a registrant’s internal control over financial reporting (“ICFR”), and will be subject to review by the registrant’s outside auditors.

With respect to disclosure of the effects of severe weather events and other natural conditions, the SEC adopted a quantitative disclosure threshold of 1% of the absolute value of stockholders’ equity or deficit at the end of the relevant fiscal year (for capitalized costs and charges) or 1% of the absolute value of income or loss before taxes for the relevant fiscal year (for expenditures and losses) to determine what information is required to be disclosed. Those disclosure thresholds are subject to de minimis thresholds for the aggregate amount of both expenditures expensed ($100,000 for the relevant fiscal year) and capitalized costs incurred ($500,000 for the relevant fiscal year) resulting from severe weather events and other natural conditions. The SEC stated that providing a bright-line standard is intended to simplify compliance compared to a more principles-based standard, with the goal to reduce underreporting and encourage comparability and consistency over time.

Examples of required disclosure include expenses, losses, capitalized costs or charges to restore operations, relocate assets or operations affected by a severe weather event or other natural condition, retire affected assets, replace or repair affected assets, recognize an impairment charge for, or impairment loss on, affected assets or otherwise respond to the effect that a severe weather event or other natural condition had on business operations. The Final Rule also clarifies that a registrant is not required to make a determination that a severe weather event or other natural condition was caused by climate change in making the disclosure related to such severe weather event or other natural condition.

As noted above, registrants should be aware that Regulation S-X disclosures may need to be considered when making materiality determinations that are required by Regulation S-K. For example, if a registrant experiences what it determines to be a severe weather event that meets the 1% threshold pursuant to Regulation S-X, it will also need to consider whether that event is, for example, an acute physical risk that has or is reasonably likely to have a material impact on the registrant.

Carbon Offsets and RECs

If carbon offsets or Renewable Energy Certificates (“RECs”) have been used as a material part of a registrant’s plan to achieve its disclosed climate-related targets or goals, the Final Rule requires registrants to disclose (i) the aggregate amount of carbon offsets and RECs expensed, (ii) the aggregate amount of capitalized carbon offsets and RECs recognized and (iii) the aggregate amount of losses incurred on the capitalized carbon offsets and RECs.

Financial Estimates and Assumptions

The Final Rule requires a registrant to disclose whether the estimates and assumptions used to produce the consolidated financial statements were materially impacted by risks and uncertainties associated with, or known impacts from, (i) severe weather events or natural conditions and (ii) any climate-related targets or transition plans disclosed by the registrant. If so, the Final Rule requires the registrant to provide a qualitative description of how the estimates and assumptions were impacted by such factors.

Inclusion of Climate-Related Metrics in the Financial Statements

The climate-related metrics that are required to be disclosed in the registrant’s financial statements will need to be (i) included in the scope of any required audit of the financial statements in the relevant filing; (ii) subject to audit by an independent registered public accounting firm, in which Public Company Accounting Oversight Board (“PCAOB”) auditing standards apply; and (iii) within the scope of the registrant’s ICFR. This approach, according to the SEC, enhances the reliability of the proposed financial statement metrics. While recognizing concerns from commenters about applying PCAOB standards, the SEC asserted that the modifications made to narrow the scope of the Final Rule should mitigate such concerns.

Scope 1 and Scope 2 GHG Emissions

In a significant shift from the Proposed Rule, the Final Rule requires only large accelerated filers and accelerated filers that are not smaller reporting companies or emerging growth companies to disclose, if material, their “Scope 1” and “Scope 2” GHG emissions. GHG emissions must be disclosed for their most recently completed fiscal year and, to the extent previously disclosed, for the historical fiscal year(s) included in a filing.

In response to commenter concerns regarding the timing for compliance with GHG emissions disclosure requirements, the Final Rule provides that GHG emissions disclosure required to be included in an annual report on Form 10-K may be incorporated by reference from the registrant’s quarterly report on Form 10-Q for the second fiscal quarter of the fiscal year in which such annual report is due, or may be included in an amended Form 10-K no later than the due date for such Form 10-Q. For FPIs, GHG emissions disclosure required to be disclosed in an annual report on Form 20-F may be disclosed in an amendment to Form 20-F, which will be due no later than 225 days after the end of the previous fiscal year.

Any GHG emissions disclosure required to be included in a registration statement pursuant to the 1933 Act and the 1934 Act must be provided for the most recently completed fiscal year that ended at least 225 days prior to the date of effectiveness of the registration statement.

Debevoise Insight

In the adopting release, the SEC notes that, to the extent Scope 1 and/or Scope 2 GHG emissions disclosures are required by the Final Rule, registrants may avail themselves of Rule 409 of the 1933 Act and Rule 12b-21 of the 1934 Act, which provide accommodations for information that is unknown and not reasonably available, if the conditions of the applicable rule are met.

Consider, however, the need to make such disclosures if an offering is planned or possible and all material information must be disclosed.

Emissions Definitions

The definitions of GHG emissions are substantially similar to those in the GHG Protocol established by the World Resources Institute and the World Business Council for Sustainable Development (the “GHG Protocol”) and include carbon dioxide, methane, nitrous oxide, nitrogen trifluoride, hydrofluorocarbons, perfluorocarbons and sulfur hexafluoride. For purposes of both the Final Rule and the GHG Protocol, Scope 1 GHG emissions include direct emissions from operations that are owned or controlled by the registrant and Scope 2 GHG emissions cover indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the registrant.

Calculating Emissions Disclosures

For both Scope 1 and Scope 2 GHG emissions, the Final Rule requires a registrant to disclose the emissions separately, each expressed in the aggregate, in terms of metric tons of carbon dioxide equivalent. Additionally, if any constituent GHG within the disclosed aggregate emissions is individually material, a registrant must disclose such constituent GHG disaggregated from the other gases. This is a change from the Proposed Rule, which would have required disaggregated disclosure for all constituent GHGs, regardless of materiality. The Final Rule requires the Scope 1 and Scope 2 GHG emissions disclosure to exclude the impact of any purchased or generated offsets.

Methodology Disclosure

Registrants will be required to disclose their calculation methodology (including any emission factors used and the source of the emission factors), significant inputs and significant assumptions used to calculate GHG emissions. This includes (i) the organizational boundaries used when calculating the disclosed GHG emissions and the methods used to determine such boundaries, (ii) a brief discussion of the operational boundaries used and (iii) a brief discussion of the protocol or standard used to report GHG emissions. The Final Rule provides registrants with the flexibility to use calculation methods used by the GHG Protocol or other recognized protocols/standards, as long as registrants disclose which method is used and provide sufficient detail to allow a reasonable investor to understand such method. Registrants may use reasonable estimates when disclosing GHG emissions as long as they also describe the underlying assumptions and rationale for using such estimates.

Attestation

With respect to Scope 1 and Scope 2 GHG emissions, the Final Rule includes an attestation requirement for registrants required to provide such disclosure (i.e., large accelerated filers and accelerated filers that are not smaller reporting companies or emerging growth companies). These registrants must (i) include with their filings attestation reports that cover these emissions disclosures and (ii) provide certain information about the attestation service provider. The attestation service provider must be an expert in GHG emissions and independent of the registrant. The attestation provider need not be an accounting firm; however, the SEC confirmed that it may be the registrant’s auditor, if the auditor is an expert in GHG emissions. The attestation requirement departs from the SEC’s typical practice for disclosures required under Regulation S-K which, unlike financial statements prepared in accordance with Regulation S-X, generally are not reviewed or audited by an independent expert.

Debevoise Insight

Under the Final Rule, a GHG emissions attestation provider will not be considered independent if such attestation provider is not, or a reasonable investor with knowledge of all relevant facts and circumstances would conclude that such attestation provider is not, capable of exercising objective and impartial judgment on all issues encompassed within the attestation provider’s engagement. In the adopting release, the SEC notes that although the independence requirements for GHG emissions attestation providers under the Final Rule are not the same as the independence requirements for financial statement auditors under Rule 2-01 of Regulation S-X, guidance and staff interpretations regarding Rule 2-01 may be a useful starting point for registrants when considering questions and issues that may arise regarding a GHG emissions attestation provider’s independence.

Additionally, changes in a registrant’s attestation provider trigger requirements to disclose certain facts relating to the change, including any disagreements between the attestation provider and the company regarding GHG emissions disclosure or other issues. These requirements are modeled on SEC rules regarding changes in a company’s auditor.

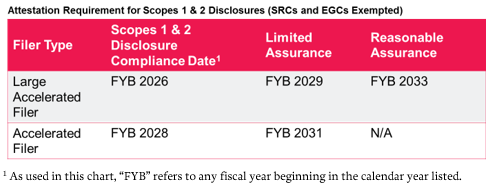

The attestation requirements will be phased in according to the following timetable. The minimum level of assurance required will be “limited assurance” (i.e., “negative assurance” that no material misstatement or omission of fact was found after a review, which is equivalent to the level of assurance provided over a registrant’s interim financial statements included in a Form 10-Q). Eventually, large accelerated filers will be required to obtain an attestation report at the “reasonable assurance” level (which the adopting release notes is equivalent to the level of assurance provided in an audit of a registrant’s consolidated financial statements included in Form 10-K).

The Final Rule requires any registrants that are not subject to Scope 1 and Scope 2 GHG emissions disclosure requirements but who nevertheless voluntarily include such disclosure in their filings to disclose certain information if such GHG emissions disclosure was subject to third-party assurance. This assurance includes, among other things, the identification of the provider for such assurance, a description of the assurance standard used and a description of the level and scope of assurance services provided.

Debevoise Insight

To the extent that the registrant’s auditor is engaged to provide an attestation report, the auditor will be required to comply with applicable, existing pre-approval requirements of audit committees. The SEC notes that, even in circumstances where the GHG emissions attestation services are not subject to a pre-approval requirement, audit committees should consider what level of involvement would be appropriate for them to take with respect to the selection and retention of attestation providers for climate-related disclosures.

Scope 3 GHG Emissions Disclosures

In a significant departure from the Proposed Rule, the Final Rule does not require registrants to disclose Scope 3 GHG emissions (all other indirect GHG emissions that occur in the upstream or downstream activities in the registrant’s value chain). In the adopting release, the SEC stated it was not adopting the requirement to disclose Scope 3 GHG emissions at this time due to, among other things, “questions about the current reliability and robustness of the data associated with Scope 3 GHG emissions.”

Debevoise Insight

Although the Final Rule does not specifically require registrants to disclose Scope 3 GHG emissions, there may be circumstances in which other provisions of the Final Rule result in such disclosure. For example, if a registrant adopts a target which relates to Scope 3 GHG emissions, Scope 3 GHG emissions disclosure may be required to describe the progress the registrant makes towards the target or because achieving the target involves material costs for the registrant.

Additionally, other rules and regulations, including pursuant to U.S. Environmental Protection Agency regulations, California’s climate disclosure rules and the CSRD, may require a registrant to disclose Scope 3 GHG emissions outside of a registrant’s SEC filings.

Impacts of Climate-Related Risks (Qualitative Disclosure)

The Final Rule requires qualitative disclosure of any climate-related risks identified by a registrant that have had, or are reasonably likely to have, a material impact on the registrant, including on its strategy, results of operations or financial condition, and which may manifest over the short or long term.

While the Proposed Rule included references to short, medium and long-term periods, the Final Rule only distinguishes between short-term (i.e., the next 12 months) and long-term (i.e., beyond the next 12 months). The SEC noted that this temporal standard is generally consistent with existing MD&A disclosure requirements, which may ease the burden on registrants in crafting this disclosure. As noted above, the prospective materiality determination required to be made regarding climate-related risks is also similar to what is generally required when preparing MD&A disclosure.

The SEC’s definition of “climate-related risks” is substantially similar to that recommended by the Task Force on Climate-Related Financial Disclosures. Specifically, the Final Rule defines climate-related risks as “the actual or potential negative impacts of climate-related conditions and events on a registrant’s business, results of operations, or financial condition.” Such climate-related risks may be physical (i.e., risks in connection with weather events or trends) or transition risks (i.e., risks in connection with the transition to a low-carbon economy).

Under the Final Rule’s definition, physical risks include “both acute risks and chronic risks to the registrant’s business operations.” Acute risks “are event-driven and may relate to shorter term severe weather events, such as hurricanes, floods, tornadoes, and wildfires, among other events” while chronic risks “relate to longer term weather patterns, such as sustained higher temperatures, sea level rise and drought, as well as related effects such as decreased arability of farmland, decreased habitability of land, and decreased availability of fresh water.”

Transition risks are defined as “the actual or potential negative impacts on a registrant’s business, results of operations, or financial condition attributable to regulatory, technological, and market changes to address the mitigation of, or adaptation to, climate-related risks, including such nonexclusive examples as increased costs attributable to changes in law or policy, reduced market demand for carbon-intensive products leading to decreased prices or profits for such products, the devaluation or abandonment of assets, risk of legal liability and litigation defense costs, competitive pressures associated with the adoption of new technologies, and reputational impacts (including those stemming from a registrant’s customers or business counterparties) that might trigger changes to market behavior, consumer preferences or behavior, and registrant behavior.”

Debevoise Insight

Issuers are expected to assess whether they have material transition risk if they have significant operations in a jurisdiction that has made a GHG emissions reduction commitment.

For physical and transition risks that are reasonably likely to have a material impact on the registrant, the Final Rule requires certain descriptions of the nature of such risks and their categorizations; however, the required items are less prescriptive than those of the Proposed Rule. For physical risks, registrants must categorize the risk as an acute or chronic risk and include the geographic location and nature of the properties, processes or operations subject to the physical risk. For transition risks, registrants must include an assessment of whether the risk relates to regulatory, technological, market (including changing consumer, business counterparty and investor preferences), liability or other transition-related factors, as well as how these factors would impact the registrant.

The Final Rule also requires disclosure of actual and potential material impacts of climate-related risks identified by the registrant on the registrant’s strategy, business model and outlook. This includes, but is not limited to, disclosure of these impacts on the registrant’s business operations, products or services, suppliers, purchasers or counterparties to material contracts, activities to mitigate or adapt to climate-related risks, research and development expenditures and all other significant changes or impacts.

Risk Management Disclosure

If the registrant identifies a material climate-related risk, the Final Rule requires disclosure of a registrant’s process for identifying, assessing and managing such material climate-related risks and whether and how any such processes are integrated into the registrant’s overall risk management system. Practitioners will recognize the language of this requirement from the SEC’s recently adopted cybersecurity risk management disclosure, which mandates similar disclosure for cybersecurity risks. In a change from the Proposed Rule, and also different from the cybersecurity disclosure rule, the Final Rule includes a materiality qualifier: if a registrant has not identified a material climate-related risk, no disclosure is required.

Debevoise Insight

Registrants should be mindful of including disclosure regarding their processes for identifying, assessing and managing material climate-related risks if no such material climate-related risks have been identified. While including risk oversight disclosure may be viewed as proactive, it could raise questions as to why the registrant is providing risk oversight disclosure when it has determined that it is not subject to material climate-related risks.

In response to concerns that the Proposed Rule’s risk management disclosure would require registrants to address items that may not be relevant to their particular business or industry, the Final Rule removed several prescriptive elements. While the Proposed Rule included specific items that a registrant would be required to address, if applicable, such as how the registrant determines the relative significance of climate-related risks compared to other risks or how the registrant considers existing or likely regulatory requirements, the Final Rule allows a registrant to determine which factors are most significant based on its particular facts and circumstances.

Aside from identifying, assessing and managing risks, registrants must also disclose how they will manage identified climate-related risks, including deciding (i) whether to mitigate, accept or adapt to a particular risk and (ii) how to prioritize certain climate-related risks. The Final Rule did not retain the proposed requirement for registrants to disclose how they determine how to mitigate any high-priority risks.

Corporate Governance Disclosures

The Final Rule requires registrants to disclose information about the oversight and governance of climate-related risks by, if applicable, both the registrant’s board of directors and management. In response to commenter concerns, the Final Rule streamlines the enumerated disclosure elements that were initially proposed and dispenses with some of the prescriptive elements of the Proposed Rule (including that registrants identify specific members of the board responsible for climate-related oversight or describe the expertise in climate-related risks of any members of the board members). In the adopting release, the SEC noted that the corporate governance information required by the Final Rule is intended to provide investors with the information they need to understand and evaluate a registrant’s oversight arrangements, if any are in place, and to make informed investment decisions in light of their investment objectives and risk tolerance. Similar to the climate risk management disclosure, practitioners will recognize the elements of the required climate corporate governance disclosure as being comparable to disclosure relating to oversight of cybersecurity risks.

Board Oversight

The Final Rule requires disclosure of the board’s oversight of climate-related risks, including, as applicable:

- The identification of any board committee or subcommittee responsible for the oversight of climate-related risks;

- A description of the processes by which the board or such committee or subcommittee is informed about such risks; and

- If a climate-related target or goal or transition plan has been disclosed pursuant to the requirements of the Final Rule, a description of whether and how the board oversees progress against the target or goal or transition plan.

Management Responsibility

The Final Rule requires disclosure of management’s role in assessing and managing material climate-related risks, including, as applicable:

- Whether and which management positions or committees are responsible for assessing and managing climate-related risks and the relevant expertise of such position holders;

- The processes by which such positions or committees assess and manage climate-related risks; and

- Whether such positions or committees report information about such risks to the board or a committee or subcommittee of the board.

Consistent with the board disclosures, the above disclosures are not required for registrants that do not engage in the oversight of material climate-related risks, including for those that do not identify any material climate-related risks.

Debevoise Insight

The adopting release clarifies that the SEC does not intend for the corporate governance disclosure requirements to shift governance practices and that the focus of the disclosure requirements is on registrants’ existing or developing climate-related risk governance practices.

Even so, prior to making disclosures about management responsibilities and board oversight, we expect that many registrants will institute a regular cadence for reporting climate-related risks to the board and for management communications to the board to support the disclosure.

Registrants should consider how best to describe management’s climate-related expertise and training, if any, in response to the SEC’s non-exhaustive list of items to consider when describing management’s role in assessing and managing climate-related risks.

Registrant Climate Policy-Specific Disclosures

The Final Rule requires disclosures on climate-related targets and goals, transition plans, scenario analyses and internal carbon pricing, to the extent that these tools are used by the registrant.

Climate-Related Targets and Goals

If a registrant has set any climate-related targets or goals and such climate-related targets or goals have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations or financial condition, the Final Rule requires the registrant to provide certain information about those goals. Examples of goals covered include those established in line with climate-related treaties, laws, regulations and policies. Specifically, the disclosure should include information necessary to an understanding of the material impact or reasonably likely material impact of the goals, including, but not limited to, descriptions of:

- The scope of activities included in the target;

- The unit of measurement;

- The defined time horizon by which the target is intended to be achieved and whether the time horizon is based on one or more goals established by a climate-related treaty, law, regulation, policy or organization;

- The defined baseline time period and emissions against which progress will be tracked; and

- How the registrant intends to meet its climate-related targets or goals (in a qualitative manner).

The Final Rule has been revised so that the items listed above are non-exclusive examples of information that a registrant must disclose if necessary to an understanding of the material impact or reasonably likely material impact of any disclosed targets or goals.

Each fiscal year, registrants who have previously disclosed targets or goals must also update their disclosure by describing any actions taken during the past year to achieve those targets or goals, including relevant data to indicate any progress made. This disclosure should include a discussion of any material impacts to the registrant’s business, results of operations or financial condition as a direct result of the targets or goals and qualitative and quantitative disclosure of any material expenditures and material impacts on financial estimates and assumptions as a direct result of the targets or goals.

If a registrant has used carbon offsets or RECs as a material component in its plan to achieve climate-related targets or goals, it is required to disclose (i) the amount of carbon reduction represented by the offsets or the amount of generated renewable energy represented by the RECs, (ii) the nature and source of the offsets or RECs, (iii) a description and location of the underlying projects, (iv) any registries or other authentication of the offsets or RECs and (v) the cost of the offsets or RECs.

The SEC noted in the adopting release that such information is intended to help investors better understand the potential financial impacts on a registrant associated with pursuing its climate-related targets or goals, as well as how well the registrant is managing its identified climate-related risks.

Transition Plan

The Final Rule requires disclosure of a registrant’s transition plan (if any) to manage a material transition risk. The Final Rule defines a “transition plan” as a strategy and implementation plan to reduce climate-related risks. Such a plan may include reducing GHG emissions in line with a registrant’s own commitments or commitments of jurisdictions within which it has significant operations.

If a registrant has adopted a transition plan, the Final Rule requires it to:

- Describe the plan;

- Include quantitative and qualitative disclosure of material expenditures incurred and material impacts on financial estimates and assumptions as a direct result of the transition plan disclosed; and

- Update its disclosure about its transition plan annually in its Form 10-K or 20-F, as applicable, by describing the actions taken during the year to achieve the plan’s targets or goals, including how such actions have impacted the registrant’s business, results of operations or financial condition.

Unlike the Proposed Rule, the Final Rule does not enumerate transition risks and factors related to those risks that must be disclosed.

Scenario Analysis

If a registrant uses scenario analysis to assess the impact of climate-related risks on its business, results of operations or financial condition and, if based on the results of such analysis, a registrant determines that a climate-related risk is reasonably likely to have a material impact on its business, results of operations or financial condition, the Final Rule requires the registrant to:

- Describe each such scenario, including a brief description of the parameters, assumptions and analytical choices used; and

- Describe the expected material impacts, including the financial impacts, on the registrant under each such scenario.

In a change from the Proposed Rule, the Final Rule does not require a registrant to disclose “any” analytical tool used, and instead requires disclosure only if scenario analysis is used.

The Final Rule defines scenario analysis as a tool used to consider how, under various possible future climate scenarios, climate-related risks may impact a registrant’s operations, business strategy and consolidated financial statements over time. In the adopting release, the SEC explains that registrants might use scenario analysis to assess their climate-related risk exposure. The SEC also notes that, while the disclosures are intended to help investors evaluate the resilience of the registrant’s business strategy, the Final Rule does not mandate the use of scenario analysis.

Carbon Price

If a registrant uses internal carbon pricing, the Final Rule requires the registrant to disclose certain information about the internal carbon price. However, in a departure from the Proposed Rule, the disclosure is required only if the use of internal carbon pricing is material to how the registrant evaluates and manages a climate-related risk it has identified as having materially impacted or which is reasonably likely to have a material impact on the registrant pursuant to Item 1502 of Regulation S-K. If applicable, the registrant must disclose for all internal carbon prices, in its reporting currency:

- The price per metric ton of carbon dioxide equivalent;

- The total price and how it is estimated to change over time; and

- The boundaries for measurement of overall carbon dioxide emissions (if materially different from those used in the GHG emission disclosures).

The Final Rule defines an internal carbon price as “an estimated cost of carbon emissions used internally within an organization.” If a registrant uses more than one internal carbon price, the registrant must provide disclosures for each and disclose its reasons for using different prices. The adopting release notes that carbon pricing can be a key data point with which investors evaluate how a registrant is managing climate-related risks and the effectiveness of its business strategy to mitigate or adapt to such risks.

Liability and Enforcement Activity

Liability and the Private Securities Litigation Reform Act (“PSLRA”) Safe Harbor

By requiring that climate-related disclosures be made as part of reports and registration statements filed with the SEC, the Final Rule creates potential liability for registrants under both the 1933 Act and 1934 Act. Registrants will thus be subject to the broad anti-fraud provisions of Section 10(b) of the 1934 Act and Rule 10b-5 thereunder, which prohibit fraudulent and deceptive practices, as well as untrue statements or omissions of material facts, made in connection with securities. As exhibited in the recent high-profile cybersecurity enforcement case against SolarWinds, this liability may go beyond documents filed with the SEC to include public statements, press releases and other public reports. If registrants make this disclosure in registration statements—including through incorporation by reference of the 1934 Act forms affected by the new rules— they may also be subject to strict liability for false or misleading statements, even for unintentional mistakes, pursuant to Section 11 of the 1933 Act.

The Final Rule extends existing safe harbors for forward-looking statements to aspects of the disclosures (excluding historical facts) pertaining to transition plans, scenario analysis, the use of internal carbon pricing and targets and goals. Additionally, the Final Rule extends such safe harbors to applicable disclosures made by registrants in connection with certain transactions that are currently excluded from existing safe harbors for forward-looking statements (such as registrants conducting an initial public offering).

Debevoise Insight

The Final Rule does not extend the PSLRA safe harbor provision to Scope 1 and 2 GHG emissions disclosures, on the premise that “the methodologies underlying the calculation of those scopes are fairly well-established,” which may present heightened risk of private litigation.

The Final Rule also does not extend the safe harbor to Scope 3 GHG emissions, on the basis that the Final Rule does not require disclosure of Scope 3 GHG emissions. For registrants who elect to voluntarily disclose Scope 3 GHG emissions, or determine that such disclosure is required by materiality determinations, the safe harbor proposed in the Proposed Rule is not available.

Note that these statutory safe harbors do not apply to forward-looking statements included in financial statements prepared in accordance with generally accepted accounting principles (“GAAP”), including the disclosure under Article 14 of Regulation S-X called for by the Final Rule.

Prior SEC Guidance and Policy Activity on Climate Change Disclosures

The 2010 Guidance provides the SEC’s views on how pre-existing disclosure requirements under Regulation S-K apply to climate change matters. In March 2021, the SEC requested public input on issues relating to climate change disclosures. Both initiatives informed the Final Rule, which directly addressed feedback received in response to the March 2021 request for comment.

Debevoise Insight

The SEC’s 2010 Guidance remains relevant to registrants because it discusses pre-existing SEC rules that are not covered by the Final Rule, such as those pertaining to a registrant’s description of its business and certain legal proceedings, which require disclosure regarding, among other things, compliance with environmental laws and regulations. Registrants must continue to consider the 2010 Guidance as they evaluate disclosure obligations in the Description of Business, Risk Factors, Legal Proceedings, and MD&A.

Additionally, beginning in September 2021, the SEC sent comment letters requesting additional climate and ESG information to a large number of public companies. The SEC concurrently released a “Sample Letter to Companies Regarding Climate Change Disclosures” (the “Sample Letter”), which serves as an example of a potential request for information from the agency to public companies “regarding their climate-related disclosure or the absence of such disclosure.”

Debevoise Insight

The Sample Letter includes the following question:

“We note that you provided more expansive disclosure in your corporate social responsibility report (“CSR report”) than you provided in your SEC filings. Please advise us what consideration you gave to providing the same type of climate-related disclosure in your SEC filings as you provided in your CSR report.”

Since publishing the Sample Letter, the SEC has reviewed registrants’ SEC filings against their publicly available climate-related disclosures and has requested information regarding perceived discrepancies. In circumstances where registrants have responded stating that the information omitted from their SEC filings was not material, the SEC has frequently requested additional information to support the registrant’s position.

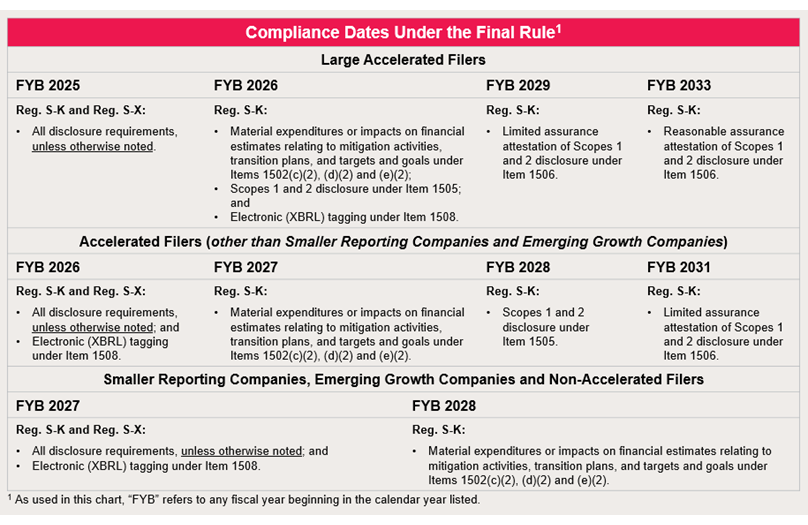

Compliance Deadlines and Next Steps

The table below indicates the compliance dates for the Final Rule, which vary depending on filer type.

Registrants should consider taking a number of actions to position themselves for the effectiveness of the Final Rule and to help mitigate potential enforcement risks. This includes:

- Comparing requirements under California climate disclosure rules and CSRD and developing a comprehensive compliance plan;

- Developing accounting policies and related ICFR, in coordination with external auditors, to enable reporting information required by Article 14 of Regulation S-X;

- Creating a materiality matrix and processes to document materiality determinations, including addressing privilege concerns;

- Assessing existing disclosure and performing a “gap” analysis;

- Doing a dry run using existing data for FY23 in order to (i) anchor “materiality” determination in quantitative data and (ii) identify gaps in available data needed to make required disclosure;

- Reviewing disclosure procedures and integrating disclosure requirements into existing processes; and

- Reviewing existing management and board risk management and oversight practices for climate-related risks against disclosure requirements to identify any changes to be made.

Debevoise Insight

Since the SEC adopted the Final Rule, seven suits challenging the Final Rule have been filed. These include two in the Fifth Circuit—one by state attorneys general and another by two energy companies—which have been consolidated, one in the Fifth Circuit by oil industry groups, one in the D.C. Circuit by the Sierra Club and three others by state attorneys general in the Sixth, Eighth and Eleventh Circuits.

Given the pending litigation, it may take some time before we have certainty as to whether and when registrants will be required to make the disclosures required by the Final Rule.

However, registrants do not have the benefit of waiting to see what the outcome of the pending litigation is as the SEC considers the transition periods to be lengthy and assumes registrants will be preparing to comply on the effective dates.

This publication is for general information purposes only. It is not intended to provide, nor is it to be used as, a substitute for legal advice. In some jurisdictions it may be considered attorney advertising.