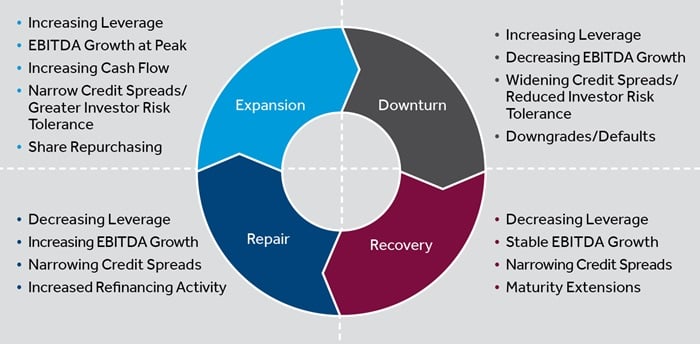

Current events, including inflation, tightening monetary policy, rapidly shifting geopolitical conditions and an aging credit cycle, are coalescing to increase transactional risk in credit markets. The aging credit cycle can bring particular challenges to finance and M&A transactions. Although economic crystal balls remain cloudy, there are steps that private equity sponsors and their portfolio companies can take to prepare should the credit cycle turn from expansion to downturn in the near to mid term (see illustration). In this article, we discuss three of the challenges such a turn in the credit cycle would bring—increased costs through capital contraction, deal execution risk, and post-transaction litigation risk—as well as best practices that, while generally prudent in any phase of the credit cycle, take on increased importance during mature expansionary periods and the transition to a downturn.

It is helpful to begin with some historical perspective. The current credit cycle has had one of the longest expansionary phases on record—lasting over a decade.For comparison, the National Bureau of Economic Research reports that the historical average length of an entire credit cycle is less than six years.As a credit cycle nears or enters the transition from its expansionary phase to a downturn, new challenges and opportunities arise. On the one hand, the cost of capital typically increases and may constrain new deal activity, the availability of (re)financing opportunities and the profitability of existing and planned investments. On the other hand, destabilized markets may offer particularly attractive investment and acquisition opportunities for courageous and adaptable investors. Investing in a late-stage market may carry a potential for strong return, but also increased risks. These risks, however, can be mitigated through advance planning and attention to detail.

Capital Contraction. In the expansionary phase of a credit cycle, overall low interest rates and a glut of investable cash put pressure on lenders to generate or maintain higher yields, incentivizing lenders to take on (or stay in) ever-riskier investments in search of the desired rate of return. When the credit cycle rolls into a downturn, conditions begin to support higher yields on relatively less risky investments. Lenders become less incentivized to support stressed credits, instead seeking either a return of capital that can be deployed on better terms elsewhere, or a more comprehensive restructuring that will reset a capital structure on higher-yield terms reflecting the new credit market. This market tightening has implications both for new capital commitments (including refinancings) and for managing existing debt facilities.

New Capital Commitments and Refinancings. New and recommitted capital is more expensive and harder to come by in a downturn. As noted above, lenders have more options for higher-yield investments. Even lenders that want to invest may be limited by internal or regulatory criteria for deploying credit into highly leveraged situations, like CLOs that are constrained by investment guidelines from deploying defensive capital to aid distressed credits. Moreover, arranging banks may price in balance sheet or claw back risk associated with the increased danger of failed syndications. In a tightening credit market, lenders can and will demand more onerous covenant packages, which in turn limit borrowers’ operational flexibility and create more opportunities for default. Particularly in transactions with a distribution to equity, financings face enhanced litigation risk. For example, creditors in bankruptcy may challenge dividends funded by debt proceeds as constructively fraudulent, claiming that the borrower was insolvent or rendered so by the transaction. The Payless Shoes and KB Toys bankruptcies provide cautionary tales.

Alternatively, lenders that are excluded from the opportunity to participate in a potential liability management transaction may subsequently seek to challenge that transaction, as a fraudulent conveyance or otherwise. This tail risk may be enough of a reason for lenders to shy away from a deal. All of this suggests that transaction activity will slow and returns to equity will decrease from expansion-period levels. Such conditions help drive the deal execution and litigation risks addressed further below.

Managing Existing Debt Facilities. A contracting credit environment also narrows borrowers’ options when trying to manage discrete liability issues like maturities, financial covenants and basket capacity. Lenders are more likely to scrutinize covenant compliance and look for opportunities to require new capital infusions and other material accommodations for amendments that would have been easily achieved in an expansionary environment. In such turbulent times, borrowers should think proactively about strategies such as:

- Tracking who owns the debt and when they acquired it, to keep an eye on evolving lender group motivations and behaviors tied to where debt is trading, and the possibility of different factions forming within a group.

- Enhancing liquidity through revolver draws before borrowing conditions become difficult to meet, or lenders themselves start to experience credit issues. Investing in covenant compliance training and materials to avoid foot faults and to educate legal, treasury and accounting personnel about potential weaknesses well in advance of defaults materializing.

Deal Execution Risk. Transactions closing at the turn of the credit cycle face two principal problems: (i) buyer’s remorse in light of more challenging or changed macro-economic conditions and (ii) difficulty in syndicating or closing financing. Sponsors and portfolio companies entering into transactions during an aging credit cycle can incorporate risk allocation strategies to address these issues.

Sponsors and their portfolio companies on the buy side should consider non-syndicated private credit financing to avoid execution risk, as well as the risk of price flex. Buyers should remain vigilant to continue to align the closing conditions in a purchase agreement and the requirements for funding financing commitments to ensure that if they are obligated to close, their lenders are obligated to fund.Working capital adjustments reflecting increases in business volatility may also be worth negotiating.

Conversely, as sellers, sponsors and their portfolio companies should seek to reduce a buyer’s optionality regarding closing the transaction. This can be accomplished by requiring a full equity backstop, as well as by watering down or eliminating closing conditions related to the go-forward business’s solvency (regardless of what the financing papers say). Additionally, in anticipation of less certainty around economic trends between signing and closing, sellers should consider the possibility of a reduction in trade credit availability and its impact on ordinary-course operating covenants.

Post-Transaction Litigation Risk. When parties close deals they later regret due to changed economic conditions, they may look to shift losses through litigation. Accordingly, portfolio companies and their directors should be prepared for a more litigious environment as the credit cycle ages.

Directors should be prepared for their actions to be scrutinized with the benefit of 20/20 hindsight, and board processes should be designed and documented accordingly.Boards should consider up-to-date information and professional recommendations before granting final approval of any deal closing to ensure that any shifts in market conditions do not undermine the business rationale for the transaction or compel a different recommendation to shareholders (if shareholder approval is required). Directors should consider different angles and test the professional advice they are given to ensure they are fulfilling their fiduciary duties. For example, the U.S. District Court for the Southern District of New York has allowed breach of fiduciary duty claims to proceed against directors who failed to consider the overall effects of a multistage transaction on the post-closing solvency of the company. Directors also should keep in mind that the enterprise value of financially distressed companies may break above equity, and their fiduciary duties may require them to consider the interests of creditors and other stakeholders when assessing potential transactions.

Similarly, boards and management should be mindful of communications and disclosures made to employees and other minority shareholders receiving equity in potential transactions. The likelihood of litigation increases when economic changes occur between signing and closing a deal if the relative risks borne by the parties no longer align with what is in public disclosures or communications. This risk is particularly acute in the turbulent conditions following a shift in the credit cycle and may require near-real-time updates to ensure recipients timely receive all information relevant to their investment decisions.

Transactions involving insolvent companies may be unwound or the proceeds clawed back under certain circumstances. For example, a debtor in bankruptcy may seek to unwind the transfer of assets or the incurrence of liabilities on the basis that it was insolvent at the time or was rendered insolvent by the deal, and that it received less than reasonably equivalent value in exchange (like the leveraged dividends noted above). A range of other insolvency-related litigation may also arise, including preference actions, efforts to recharacterize debt investments as equity or sale transactions as loans, and the judicial subordination of debt for inequitable conduct. Transactions can be structured to account for and mitigate such risks through a combination of financial opinions, corporate structure and market testing.

In light of rapidly shifting geopolitical and economic conditions, sponsors and their portfolio companies would be well-advised to prepare for the potential risks and corresponding opportunities associated with a change in the credit cycle.