Crypto Unchained: The SEC’s Pivotal Interpretive Release

On March 17, 2026, the SEC issued an interpretive release (the “Release”) regarding the application of the federal securities laws to certain crypto assets and transactions involving crypto assets, based primarily on whether they are subject to an “investment contract” under Howey. The Release states that the SEC will administer the federal securities laws consistent with that interpretation. It also includes a statement endorsed by the Commodity Futures Trading Commission (the “CFTC”) that certain non-security crypto assets could meet the definition of “commodity” under the Commodity Exchange Act and supersedes the SEC staff’s 2019 digital asset framework and certain prior SEC or staff statements on digital collectibles, protocol mining and protocol staking.

The Release addresses three principal areas:

- Token Taxonomy. The Release classifies crypto assets into five categories: digital commodities, digital collectibles, digital tools, stablecoins and digital securities but notes that some crypto assets may fall outside those categories or have hybrid characteristics.

- Investment Contract Formation. The Release explains when a crypto asset may qualify as an investment contract based on investor reliance on an issuer’s efforts and when it may no longer qualify once those expectations are no longer tied to the asset.

- Common Crypto Activities. The Release concludes that protocol mining, protocol staking, wrapping and certain airdrops do not involve the offer and sale of securities.

The Release is intended to give market participants a more usable framework for analyzing how the federal securities laws apply to crypto assets and common crypto activities. Market participants should note that the Release does not diminish the application of the federal securities laws’ anti-fraud provisions. Even where a non-security crypto asset separates from an investment contract, the issuer remains potentially liable for material misstatements or omissions made in connection with the investment contract during its existence.

Finally, it is important to recognize that as an interpretive statement, the Release is not binding on courts interpreting the definition of “security” under the federal securities laws in the context of civil litigation. In that respect, the Release may substantively affect regulatory enforcement posture without fully resolving litigation exposure.

Nevertheless, the Release represents an important step in the SEC’s approach to crypto assets and has several important practical implications for market participants. Further SEC action is expected, including proposals on capital-raising, exemptions, safe harbors and disclosures, as well as additional guidance and potential rulemaking in coordination with other regulators.

For more information, see Debevoise Insights.

Chairman Atkins’s Three-Pillar “ACT” Strategy for SEC Reform

On March 19, 2026, Chairman Paul S. Atkins delivered his remarks at the annual SEC Speaks conference. Chairman Atkins framed the SEC’s agenda around a three-pillar “ACT” strategy. First, Chairman Atkins noted that the SEC will Advance rules to reflect how markets operate today in comparison to its prior regulation-by-enforcement approach, particularly regarding crypto. Second, the SEC will Clarify regulatory jurisdiction to streamline oversight and unlock innovation. Specifically, Chairman Atkins discussed the memorandum of understanding signed by the SEC and the CFTC to align regulatory definitions, coordinate oversight and facilitate data-sharing. Third, the SEC will Transform the rulebook by eliminating burdensome or impractical requirements. With this, the SEC’s Division of Corporation Finance is actively engaged in its first-principles review of disclosure requirements, focusing on materiality, with comments due on April 13 for the Regulation S-K reform effort, and the Division of Enforcement is focusing on fraud, market manipulation and abuses of trust rather than technical violations that do not harm investors. He further noted that, following a court remand of the SEC’s securities lending and short sale rulemakings, SEC staff had been directed to recommend a reporting regime that balances policy goals with reporting burdens.

For more information, see Prepared Remarks Before SEC Speaks.

It’s Time for a Prediction Markets MNPI Policy

Prediction markets are platforms on which users buy or sell so-called “event contracts” tied to the occurrence or non-occurrence of future events, offering event contracts based on elections, weather, sports, commodity prices, economic data releases and similar events. Since the beginning of 2026, the CFTC has asserted its exclusive jurisdiction and rapidly intensified its scrutiny of these markets. On March 31, 2026, CFTC Enforcement Director David Miller signaled that insider trading in the prediction markets is the CFTC’s Division of Enforcement’s top priority and that the division will “aggressively detect, investigate and, where appropriate, prosecute insider trading in the prediction markets.” The CFTC has also successfully pursued insider trading cases involving derivatives under Rule 180.1, its broad antifraud and antimanipulation rule, which provides a ready template for prediction markets cases.

The misuse of material nonpublic information (“MNPI”) in connection with prediction markets trading poses an emerging compliance risk for asset managers, broker-dealers and public companies, which may need to supplement existing policies and procedures to address this risk. Registrants typically maintain sophisticated controls for brokerage accounts, securities preclearance and restricted lists, but event contract accounts may be outside those surveillance systems. As such, policies and procedures that prohibit the misuse of MNPI solely in connection with securities trading should be expanded to address all event contracts, with an explicit reference to prediction markets. Because prediction markets do not involve “securities” and because the breadth of prediction markets may create scenarios where a wider range of employees could potentially misuse information, insider trading policies may not, on their own, be the most effective way to address these risks. Companies should therefore consider revising their codes of conduct to prohibit misuse of MNPI. Asset managers or broker-dealers that seek to use prediction markets data in connection with trading strategies should also consider enhancing their policies and procedures governing the documentation of trading decisions.

When revisiting policies, companies should consider including the following elements:

- define the terms “prediction markets” and “event contracts”;

- define the controls framework of personal prediction markets accounts, including whether to require disclosure, require pre-clearance, restrict certain activity or prohibit it altogether;

- prohibit employees from misusing confidential, proprietary or material nonpublic information relating to the company or obtained through the course of their employment or affiliation with the company in connection with prediction markets trading;

- consider whether blackout periods and pre-clearance requirements should apply to trades on prediction markets or whether heightened restrictions or prohibitions should apply to employees with access to certain information;

- reevaluate trading policies holistically relating to trading in other non-securities contracts that are otherwise regulated by the CFTC; and

- update employee MNPI training and certification processes to address prediction markets-related policies and procedures.

For more information, see Debevoise Insights.

Activism in the Insurance Industry

Activism remains a persistent and increasingly important feature of the landscape for publicly traded insurance groups. Activist campaigns in recent years fall into two broad categories: institutional investors holding long-term positions and transaction-focused investors such as hedge funds and special situations funds. The former tend to focus on longer-term and often complex strategies for increasing the value of their investments; the latter are more likely to build positions (long or short) quickly and pressure companies to respond to negative news, take steps to deliver short-term value or engage in strategic transactions.

State insurance regulation continues to shape the parameters within which activist investors operate, including through approval requirements applicable to acquisitions of “control” positions, but, in practice, activists have demonstrated their ability to exert meaningful influence without taking such a position. State insurance law should not be viewed as a complete shield against the influence of activists, and companies should not expect that insurance regulators will take sides in an activist campaign. Accordingly, insurance group boards should regularly consider and take advice on the potential exposure of their companies to activist pressure, and companies should continuously invest in their relationships with insurance regulators with transparency and regular engagement.

Insurance companies were subject to 23 campaigns in 2025, which reflect familiar themes such as short-sellers establishing positions and publishing negative reports, long-term investors pressuring companies to pursue new strategies, a continued moderation in ESG-driven activity and, in some cases, hostile takeover proposals.

Insurance companies, like other companies, should prepare for activist campaigns “on a clear day.” In addition to evaluating a company’s performance relative to its peers, companies should articulate and execute business strategies that are understood by the market, prepare clear communications that address the interests of key stakeholders, have a program in place for consistent engagement with shareholders and review bylaws and other documents to ensure that the company is well-positioned to respond to activists. As the U.S. Property & Casualty market softens, conditions may be ripe for activist activity in this sector.

For more information, see Debevoise Insights.

Preparing for AI Whistleblowers – 2026 Update

Regulators have continued to prioritize AI-related conduct and AI whistleblower risks have accelerated exponentially since 2024 due to enterprise AI tool development and deployments, specifically agentic AI in spite of reduced SEC and Department of Justice (“DOJ”) enforcement activity and lower whistleblower awards. Accelerating AI adoption, particularly agentic AI, combined with growing public skepticism is increasing the likelihood of internal complaints and external reporting.

Companies face overlapping risks from SEC scrutiny of AI disclosures, DOJ incentives that encourage rapid external reporting and civil retaliation claims under state law, which, combined, heighten pressure to respond both quickly and carefully to AI-related whistleblower concerns. Specifically, the SEC prioritizes AI through its Cyber and Emerging Technologies Unit, which expressly targets fraud involving emerging technologies, and the Division of Examinations’ FY2026 priorities, which specifically identify registrants’ use of AI technologies and trading algorithms. While there has been a moderation in enforcement activity during the current administration, the statute of limitations for fraud will outlast this administration, and companies could face risk from AI whistleblowers under future administrations.

Companies deploying AI should consider adopting the following measures for updating whistleblower policies and procedures to manage AI risk:

- substantiating AI capability claims;

- accelerating internal response timelines;

- training managers involved in AI on relevant whistleblower protections and escalation procedures;

- reviewing all employee or contractor agreements for compliance with the Rule 21F-17 requirement not to impede individuals from contacting the SEC to report a possible securities law violation;

- addressing complaints properly;

- taking concerns seriously;

- protecting whistleblower anonymity;

- providing context for decisions;

- ensuring that the designated investigation team has the necessary AI experience to evaluate the whistleblower’s allegations or has access to consultants who can assist in that evaluation.

For more information, see Debevoise Insights.

Agent Washing: Disclosure Risks in the Emerging Market for AI Agents

Agent washing refers to companies calling an AI tool “agentic” when it is really just conventional automation or only has limited generative AI functionality, as well as companies overstating the degree of autonomy, reliability or business impact of an AI agent or failing to sufficiently disclose the risks and uncertainties associated with using agents in consequential AI workflows. Agent washing poses a heightened risk for two main reasons. First, the term “agent” can refer to various things, ranging from a chatbot that executes one API call to a multistep system that plans, reasons, retrieves data, uses tools and takes action across enterprise applications, which makes the term attractive for marketing but creates disclosure risks. The terms “AI agent,” “AI agents” and “agentic AI” are also often used interchangeably but refer to distinct concepts, and the imprecise use of these terms may mislead clients, regulators or investors about the capabilities and autonomy of the underlying systems and compound disclosure risks. Second, AI agents are often marketed with bold or dramatic statements due to market pressure on companies to assert that they not only “use AI” but also that they have deployed AI agents that produce measurable business outcomes, creating a risk of overstating the role of agents.

Agent washing occurs in two principal contexts.

- Overstating the Existence, Autonomy or Effectiveness of Agents. Once a company links AI agents to growth, efficiency, differentiation or valuation, subsequent disclosures about technical limitations, weak adoption, incidents or poor performance can be recast by plaintiffs as evidence that earlier statements about agentic AI were false or materially incomplete. Moreover, these specific claims about agentic AI (as opposed to generalized statements about AI usage) are arguably easier for plaintiffs and regulators to test against actual functionality, failure rates and human involvement.

- Understating the Risks and Uncertainties of Agentic AI. The risk of presenting AI use as more mature, controlled, predictable or beneficial is particularly significant. AI agents can introduce a different operational profile from conventional analytics tools or even ordinary generative AI assistants, which can lead to cascading risks such as hallucinations, fabricated citations, cybersecurity risks and insufficient auditability and recordkeeping for decisions or recommendations influenced by the agent.

Companies deploying AI agents should consider the following steps in connection with building a disciplined internal process for ensuring that statements about AI agents are precise, current and grounded in evidence:

- define “agent,” “agents” and “agentic AI” internally before using the terms externally;

- substantiate claims about capability, autonomy and business impact;

- disclose material limitations and uncertainty, especially where agents are used in sensitive workflows; and

- align external statements with internal controls.

For more information, see Debevoise Insights.

Governance Considerations for Replacing External Auditors

Companies may elect to disengage their external auditors for many reasons. Regardless of the reason, a change in auditors triggers a series of governance, independence and disclosure obligations that requires careful coordination among the audit committee, management, counsel and the outgoing and newly engaged external auditors.

Audit Committee. The audit committee is directly responsible for the appointment, compensation and oversight of the company’s independent auditor under Section 301 of the Sarbanes-Oxley Act; Rule 10A-3 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”); and the applicable NYSE and Nasdaq listing standards. As such, the auditor must be formally engaged by the audit committee through an engagement letter, often signed by the company’s management, ratified by the board and, although not legally required, typically ratified by the shareholders.

Auditor Independence. The audit committee is responsible for deciding whether an audit firm will be independent during the audit engagement period. Rule 2-01 of Regulation S-X sets forth the independence requirements for auditors and states that an auditor’s independence is impaired if the auditor is not, or a reasonable investor with all relevant facts and circumstances would conclude that the auditor is not, capable of exercising objective and impartial judgment on all issues encompassed within the audit engagement.

Disclosures. When a company’s independent auditor is dismissed, resigns or declines to stand for reelection, Item 304(a) of Regulation S-K is triggered, and if a company does not simultaneously engage a new auditor, a separate reporting obligation is triggered when one is engaged. If a company’s principal independent auditor resigns, is dismissed or indicates it has declined to stand for reelection after the completion of the current audit, the company must disclose this by filing a Form 8-K under Item 4.01. Companies reporting an auditor’s departure must also comply with the process in Item 304(a)(3) and provide the former auditor with a copy of the disclosures and request a letter indicating whether it agrees with those disclosures, a copy of which must be filed as an exhibit. Item 304(a) also requires disclosure of “disagreements” between company personnel responsible for financial statement presentation and accounting firm personnel responsible for rendering the audit report and specified “reportable events,” including where the former auditor advised that necessary internal controls do not exist, it is unwilling to rely on management’s representations or be associated with the company’s financial statements, the audit scope should be significantly expanded or newly discovered information would have materially affected prior audit reports.

Capital Markets Considerations. In connection with a registered offering, a company must obtain the consent of an auditor whose report is included or incorporated by reference in the registration statement and comfort letter from the company’s independent auditor(s) for the periods included or incorporated by reference in the offering document. If an auditor change occurs in the audit engagement lookback period for a securities offering, the company must obtain consents from the former auditor and comfort letters from both the former and new auditor covering the financial statements included in the offering documents.

For more information, see Debevoise Insights.

The Division of Corporation Finance Revises CFIs on Rule 701, Rule 405, Regulation S-K and Form S-3 Eligibility

On March 6, 2026, the Division of Corporation Finance updated its Securities Act Rules Corporation Finance Interpretations (“CFIs”)—formerly known as Compliance and Disclosure Interpretations—relating to Rules 701 and 405; its Securities Act Forms CFI; and its Regulation S-K CFIs. The updated Securities Act Rules CFIs revise six questions regarding Rule 701, which provides an exemption for offers and sales of securities pursuant to certain compensatory benefit plans and contracts, and Question 203.03 on the definition of “ineligible issuer” under Rule 405. The Division of Corporation Finance also added new Questions 271.26 and 271.27 addressing disclosure obligations for options granted pursuant to plans covered by Rule 701 over three consecutive 12-month periods. New Question 101.06 on Securities Act Forms clarifies whether a company reorganizing from an LLC to a C corporation requires a new CIK number. The Division of Corporation Finance also added Question 102.06 to its Regulation S-K C&DIs confirming that failure to check the smaller reporting company (“SRC”) status box does not result in loss of SRC status or the ability to use SRC accommodations if the issuer qualifies.

On March 19, 2026, the Division of Corporation Finance also updated its CFIs on Securities Act Forms by adding a new question regarding Form S-3. New Question 116.26 clarifies that the staff will not object if a company offering securities in reliance on General Instruction I.B.1 of Form S-3 no longer meets the $75 million public float requirement following a Section 10(a)(3) update and continues to offer and sell the full amount of securities under General Instruction I.B.6 (“baby shelf”) despite exceeding the baby shelf offering limits.

For more information, see the updated CFIs here and here.

SEC Proposes to Limit Rule 15c2-11 to Equity Securities Only

On March 16, 2026, the SEC proposed amendments to Rule 15c2-11 under the Exchange Act that would formally limit the scope of the rule to equity securities only.

Under Rule 15c2-11, a broker-dealer that wishes to publish a quotation for an issuer’s securities in a quotation medium other than a national securities exchange (i.e., over-the-counter, or “OTC”) must first establish that certain information about the issuer is current and publicly available. In 2021, the SEC interpreted this rule to apply to fixed-income securities and introduced a phased compliance regime. In 2023, in response to concerns expressed by industry participants, the SEC provided exemptive relief for fixed-income securities sold in reliance on Rule 144A under the Securities Act of 1933, as amended. In 2024, the staff of the SEC’s Division of Trading and Markets issued a no-action letter addressing other categories of fixed-income securities, but this no-action letter did not encompass all non-equity securities.

Under the proposed amendment, the terms “security” and “securities” in Rule 15c2-11 would be replaced with “equity security” or “equity securities” as defined in Rule 3a11-1 under the Exchange Act. Equity security includes a broad range of equity interests and also includes crypto assets to the extent that a crypto asset is an equity security. The SEC’s current exemptive relief and no-action positions remain in effect pending adoption of a final rule.

For more information, see Debevoise Insights.

SEC Approves Nasdaq Proposal to Permit Tokenized Securities Trading Through DTC Pilot

On March 18, 2026, the SEC approved The Nasdaq Stock Market LLC’s (“Nasdaq”) proposal to amend its rules to enable the trading of securities on the exchange in tokenized form as part of a tokenization pilot program operated by the Depository Trust Company (“DTC”). Under the proposal, DTC-eligible participants may trade tokenized versions of certain equity securities and exchange-traded products that are eligible for tokenization as part of the DTC pilot. Tokenized shares would be tradable in the Nasdaq Market Center together with, or on the same order book and with the same execution priority as, traditional shares, but only if they are fungible with the traditional shares, have the same CUSIP and trading symbol, and afford the same rights and privileges. Eligible securities are limited to securities in the Russell 1000 Index and exchange-traded funds that track major indices, and Nasdaq will publish Equity Trader Alerts identifying the current list of eligible securities.

DTC-eligible participants seeking tokenized clearing and settlement must notate that preference upon entry of the order, which Nasdaq will communicate to DTC on a post-trade basis. If DTC cannot execute the tokenization preference or instruction, DTC will settle the executed order in traditional, non-tokenized form. Nasdaq stated that tokenization will not otherwise change its trading procedures and behavior.

The SEC found the proposal consistent with the Exchange Act, including Section 6(b)(5), and emphasized that its approval is limited to the DTC pilot. The proposal will become effective once DTC has established the requisite infrastructure and post-trade settlement, and Nasdaq will give at least 30 calendar days’ notice before tokenized trading begins.

For more information, see SEC Release.

Securities Law-Related Legislation

A summary of selected recent securities law-related legislation proposed in March 2026 follows:

|

Name of Bill

|

Description of Bill

|

Latest Action

|

|

H.R.7886

|

To provide federal financial regulators with clawback authority over executive compensation and additional industry prohibition and civil money penalty authority with respect to executives whose negligence caused financial loss to the applicable financial institution and for other purposes.

|

House – 03/09/2026 Referred to the House Committee on Financial Services.

|

|

S.4034

|

A bill to amend the Securities Exchange Act of 1934 to specify certain registration statement contents for emerging growth companies, to permit issuers to file draft registration statements with the Securities and Exchange Commission for confidential review and for other purposes.

|

Senate – 03/10/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

|

S.4157

|

A bill to prohibit bailouts of digital asset market participants and for other purposes.

|

Senate – 03/19/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

|

S.4170

|

A bill to amend the Securities Act of 1933 with respect to small company capital formation and for other purposes.

|

Senate – 03/24/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

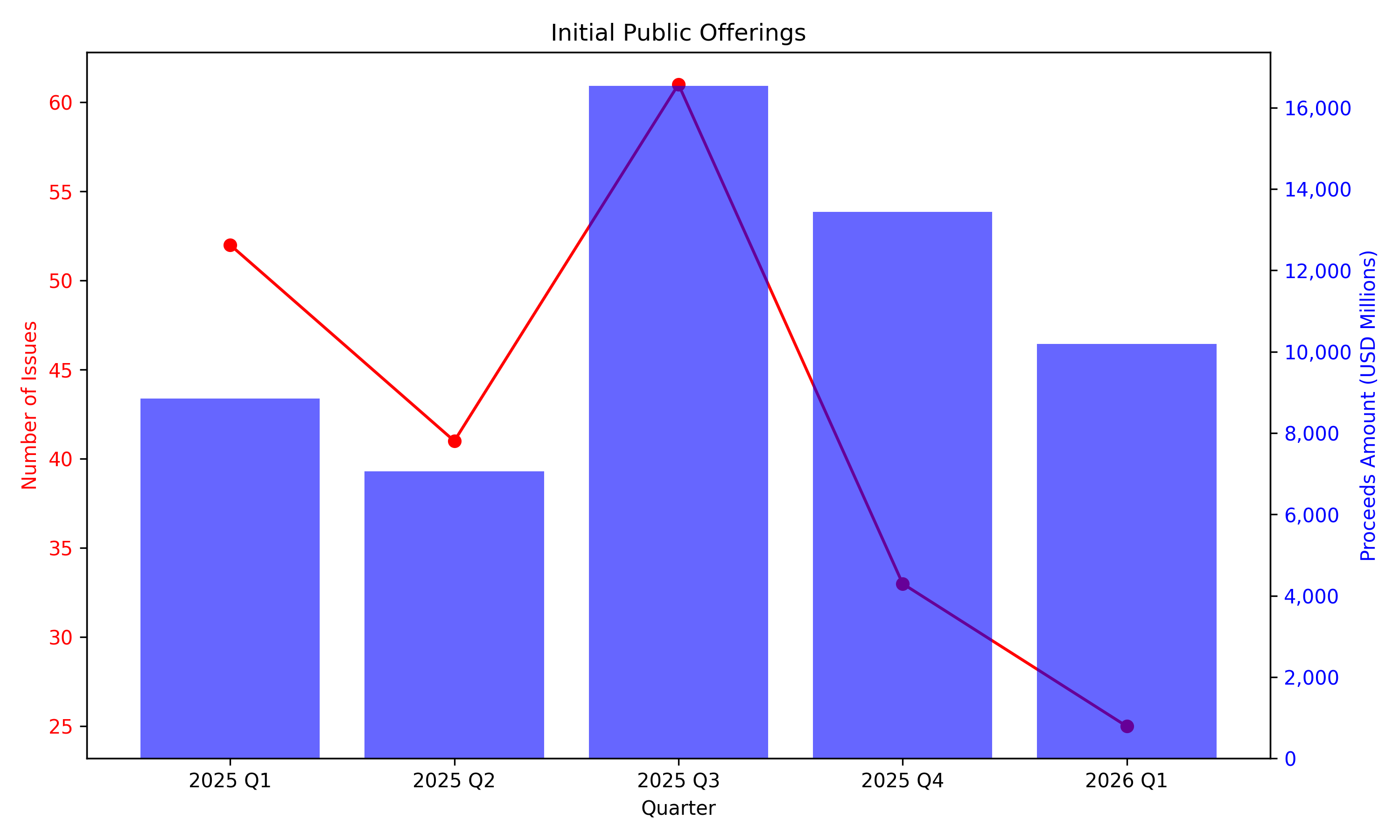

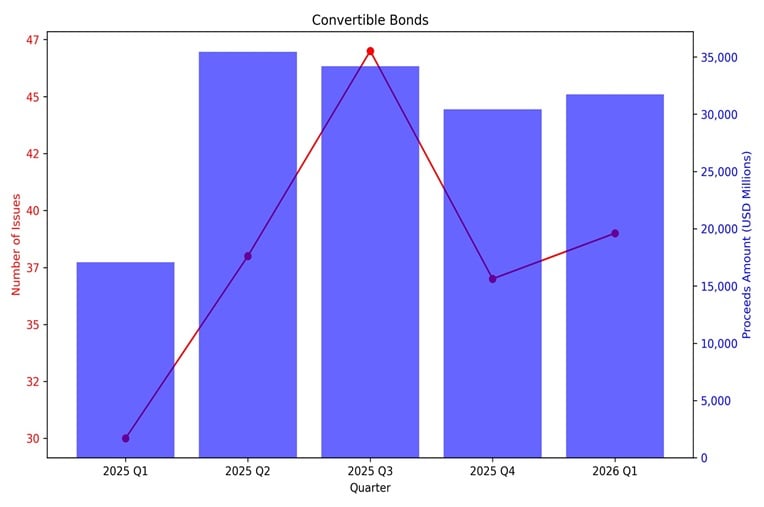

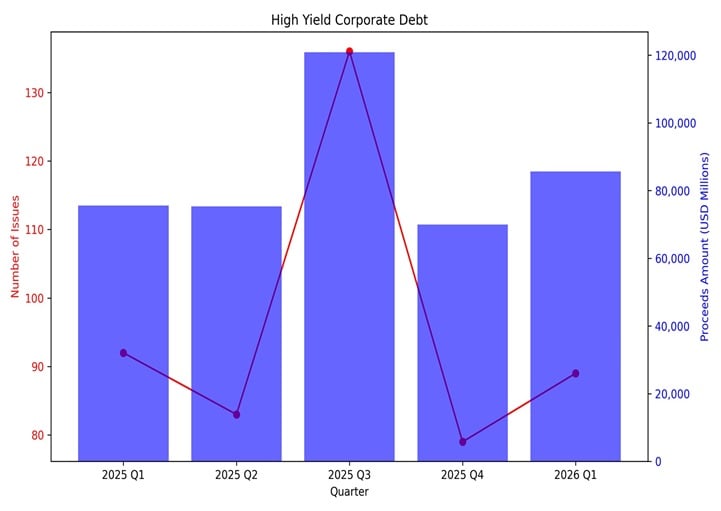

Markets At a Glance

The below market snapshot shows the volume of U.S. IPOs, follow-on offerings, investment grade corporate debt issuances, convertible bonds issuances and high-yield corporate debt issuances from the first quarter of 2025 through the first quarter of 2026.

This publication is for general information purposes only. It is not intended to provide, nor is it to be used as, a substitute for legal advice. In some jurisdictions it may be considered attorney advertising.