Key Takeaways:

- On February 20, 2026, the U.S. Supreme Court struck down the sweeping tariffs imposed under the International Emergency Economic Powers Act of 1977 (“IEEPA”). The ruling eliminates a key legal tool that the Trump administration used to justify its broadest tariff measures and limits its ability to impose future tariffs unbounded in geographic, temporal and subject-matter scope. It also opens the door to an estimated $170 billion in refunds, although the path to such refunds for most importers is not yet settled and may lead to increased disputes risk as a result of pass through issues.

- The Supreme Court’s decision changes little else about the U.S. tariff and foreign policy landscape. The same day, the Trump administration announced temporary global tariffs under Section 122 of the 1974 Trade Act and will likely continue its tariff policies under other, more established—and likely more durable—tariff authorities, including Section 232 of the 1962 Trade Expansion Act and Section 301 of the 1974 Trade Act. The decision leaves IEEPA otherwise intact in its other uses, including as the authorization for most U.S. sanctions, preserving it as a core foreign and economic security policy tool outside the tariff context.

- Companies must therefore continue to develop durable strategies to manage the consequences of a continued tariff regime that may become even more complex. These could include (i) proactively structuring contracts to allocate and manage tariff risk; (ii) implementing comprehensive supply chain assessment and due diligence frameworks to anticipate future tariffs and related financial exposure and dispute vulnerabilities; and (iii) operationalizing tariff readiness through cross-functional governance, rapid response protocols and strengthened trade-compliance controls.

In a splintered decision on Friday, February 20, 2026, six of the nine Supreme Court justices held in Learning Resources, Inc. v. Trump (consolidated with Trump v. V.O.S. Selections, Inc.) that IEEPA does not authorize the President to impose tariffs under its grant of authority to “regulate . . . importation.” The majority agreed that tariffs are an exercise of Congress’s core taxing power under Article I and that Congress did not delegate that authority to the President under a statutory interpretation of IEEPA’s terms. A narrower three-judge plurality further found that the “major questions” doctrine applied and that, under that line of decisions, IEEPA lacks the “clear congressional authorization” required to confer such economically and politically significant power as the ability to unilaterality set the scope, amount and duration of tariffs. The three dissenting justices argued that the “major questions” doctrine does not apply at all to this case for several reasons, including that it has never been used in connection with a case involving foreign affairs.

On the same day, President Trump issued a series of orders to comply with the decision, while preserving related measures and imposing a new global duty. He (i)issued an Executive Order revoking all IEEPA-based ad valorem tariffs imposed under his administration, and ordering that collection cease “as soon as practicable” and that the Customs and Border Patrol (“CBP”) modify the Harmonized Tariff Schedule; (ii) issued another Executive Order clarifying that the suspension of the de minimis exception for shipments valued at less than $800, originally enacted alongside the IEEPA tariffs, remains in effect; and (iii) signed a Proclamation imposing a 10% ad valorem import duty on all trading partners under Section 122 of the Trade Act of 1974, which took effect on February 24, 2026, and is authorized under the statute for only a 150-day period.

In this Debevoise In Depth, we address three questions arising from Learning Resources and related developments: (i) what has changed, including new constraints on the President’s ability to impose open-ended tariffs and the potential scope of IEEPA-related refund exposure; (ii) what has not changed, including the Trump administration’s broader tariff posture and the other tariff and foreign-policy tools that remain available; and (iii) what companies should consider doing now to manage the risks in the evolving tariff environment.

What Has Changed: Tariff Flexibility Modestly Narrows; Refund Complications Ensue

First, without IEEPA, the Trump administration will lose a sweeping—and unusually flexible—source of asserted authority to impose tariffs quickly by executive action, without investigations or meaningful limits as to geography, duration or subject matter. That breadth is precisely why IEEPA served as the statutory foundation for several of the administration’s core tariff measures.

As a result, even though tariffs will remain a central feature of this administration’s policy (as discussed below), companies should expect a tightening of the process and parameters. Future tariffs, assuming enactment under current U.S. trade authorities, are more likely to require lead time and be time limited, narrower in scope, and targeted to particular goods, particular countries or both.

Second, the roughly $170 billion in IEEPA-tariff refunds now in play is likely to increase near-term uncertainty for affected companies. Despite striking down the wide-ranging IEEPA tariffs, as Justice Kavanaugh’s dissent noted, the “Court says nothing today about whether, and if so how, the Government should go about returning the billions of dollars that it has collected from importers.” Precedent suggests at least two potential refund routes, but several unresolved issues remain about the precise scope and features of what will be the largest tariff refund process in U.S. history.

The first potential route is a judicially driven process, overseen by the Court of International Trade (the “CIT”). There is some precedent. In 1998, the U.S. Supreme Court held that the U.S. Government’s “harbor maintenance tax” (“HMT”) against exporters was unconstitutional. Following the Supreme Court’s decision, the CIT established a “claims resolution procedure” on remand for plaintiffs that had filed refund claims prior to the decision. Separately, affected exporters also had the option to first seek refunds directly from CBP and litigate any denials in CIT, which allowed them to avoid a two-year statute of limitations imposed on those seeking refunds directly via CIT litigation.

Before the Supreme Court’s decision in Learning Resources, over 1,500 plaintiffs had already filed CIT actions to preserve their refund claims. Those cases were largely stayed pending the Court’s ruling. As the CIT revisits those cases, those plaintiffs will likely be better positioned to seek earlier refunds, having already preserved jurisdiction, timeliness and related procedural arguments. New plaintiffs are beginning to file suits as well, but later filers may face additional hurdles and congestion in the CIT. Other importers with potential refund claims should closely monitor any decisions in these cases for guidance on how to appropriately preserve rights, comply with any refund procedures and avoid statute-of-limitations issues.

The second potential route would be through a CBP-established administrative refund process, similar to prior Section 301 and Section 232 refund cases. Given the sheer number of importers affected (over 300,000) and the amount of money implicated, tariff refund requests may overwhelm the CIT and spur calls for a separate CBP administrative process. Although the CBP has recently moved to modernize the mechanics of issuing refunds, the Trump administration has publicly signaled that whether and when tariff refunds will be paid is a question for the lower courts to resolve. Either way, potential claimants should pay close attention to CBP updates and guidance on this matter.

Importers should also expect pass-through issues to complicate refund efforts and increase exposure. If duties were passed on to buyers further down the supply chain through increased prices, the government may argue the importer did not bear the economic burden and is therefore not entitled to a refund. At the same time, downstream buyers may pursue contractual or extra-contractual claims seeking reimbursement. Outcomes will turn on contract language, pricing structure and proof of actual pass-through, and importers will often have strong defenses where prices were fixed, negotiated globally or reflected multiple cost inputs beyond tariffs. Refund-related commercial disputes therefore present a meaningful secondary risk that companies should evaluate in parallel with any refund strategy.

What Has Not Changed: Tariffs and IEEPA Remain Essential to the Administration’s Policy Toolkit

Learning Resources otherwise changes little about the Trump administration’s broad support for tariffs or its views about the related foreign policy landscape. From the outset, tariffs have been a central tool for this administration, which has invoked a range of statutory authorities to support its tariff measures. Given the Trump administration’s clear intent to continue using tariffs—and the multiple non-IEEPA statutory pathways available—tariffs are likely to remain a mainstay throughout its tenure. In addition, the Supreme Court’s decision that IEEPA does not grant the President authority to impose tariffs leaves the statute to continue as a basis for other measures imposed on national security or foreign policy grounds, such as limited embargoes in place of tariffs.

Non-IEEPA Tariff Bases

Beyond IEEPA, the Trump administration has imposed tariffs under Section 232 of the Trade Expansion Act, Section 301 of the Trade Act of 1974 and, most recently, Section 122 of the Trade Act of 1974. Looking ahead, it could also rely on other authorities—including Section 201 of the Trade Act of 1974, and Section 338 and anti-dumping and countervailing duties (“AD/CVD”) under the Tariff Act of 1930—to pursue additional tariff actions.

None of these statutory authorities afford the President the same flexibility and breadth of authority as that claimed under IEEPA. Most are more procedurally demanding and constrained by subject-matter, geographic and/or temporal limitations. And, with the exception of Sections 122 and 338—neither of which has previously been used to impose tariffs—these other bases have already withstood legal challenges, with courts affirming them as a basis for tariffs and affording deference to resulting executive decisions to impose tariffs.

Accordingly, companies should expect that tariff actions pursued outside IEEPA will generally be narrower in scope and slower to implement given the procedural and statutory constraints that apply. Those heightened requirements may also give affected parties additional avenues to challenge tariffs imposed by the Trump administration on procedural and as-applied grounds. At the same time, the same guardrails make measures adopted under these established, court-tested authorities more likely to withstand scrutiny and endure once in place.

Tariff Authorities Currently Invoked by the Administration

- Section 122 of the Trade Act of 1974. Enables the President unilaterally to implement temporary import surcharges not exceeding 15% ad valorem or for longer than 150 days to address serious balance-of-payment deficits, the depreciation of the dollar or other “fundamental international payments problems.” 19 U.S.C. § 2132. Section 122 does not require any prior investigation or procedural prerequisites for presidential action. As noted, the Trump administration invoked Section 122 in its response to Learning Resources to impose a 10% tariff on all imports, and President Trump has since further announced his intent to raise that rate to the statutory maximum of 15%. Section 122 has never been invoked because the primary intent of such tariffs was to address concerns that arose under a bygone international financial system that allowed conversion of U.S. dollars to gold at a fixed rate. We expect court challenges will follow swiftly.

- Section 232 of the Trade Expansion Act. Allows the President to impose tariffs on goods that the Secretary of Commerce determines—after an investigation—are brought into the country in “such quantities or under such circumstances as to threaten to impair the national security.” 19 U.S.C. §1862. The statute grants the President substantial discretion and specifies that “national security” may include a threat to U.S. economic welfare and domestic industrial capacity. Section 232 tariffs generally are product-specific and apply to all trading partners unless explicitly exempted.

Since 1972, U.S. courts have consistently upheld the President’s broad discretion under Section 232 to impose tariffs to protect national security. Most recently, in AIIS v. U.S. (Fed. Cir. 2020) and USP Holdings v. U.S. (Fed. Cir. 2022), the Federal Circuit upheld the first Trump administration’s Section 232 steel tariffs and found that, under Section 232, the national security “threat” need not be imminent and that the President has unreviewable discretion to accept or reject the Commerce Secretary’s findings.

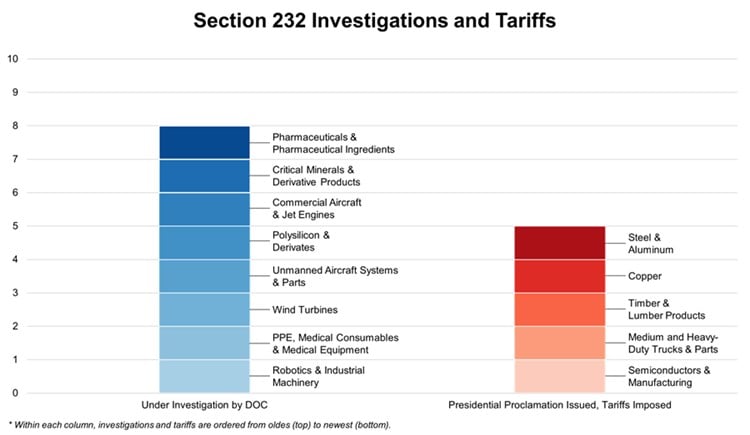

Since 2025, the Trump administration imposed Section 232 tariffs on multiple product categories, and several additional investigations are ongoing, including into pharmaceuticals, critical minerals, aircraft and others—as shown in Figure 1 below. After the Supreme Court decision in Learning Resources was published, the Trump administration announced its plan to “[m]aintain tariffs currently imposed under Section 232 of the Trade Expansion Act of 1962, and conclude ongoing investigations.”

Figure 1 - Current Section 232 Investigations and Tariffs.

Section 301 of the Trade Act of 1974. Authorizes the U.S. Trade Representative (the “USTR”)—after an investigation and subject to the President’s direction—to impose duties over goods from foreign countries that have denied U.S. rights under trade agreements or “burden[ed] or restrict[ed]” U.S. commerce in a manner that is “unjustifiable,” “unreasonable” or “discriminatory.” 19 U.S.C. §§2411-2420. U.S. courts have addressed Section 301 measures in the context of challenges to modifications of said measures under Section 307 of the Trade Act of 1974 and have afforded “substantial deference” to the USTR so long as they follow the requisite procedural and evidentiary processes.

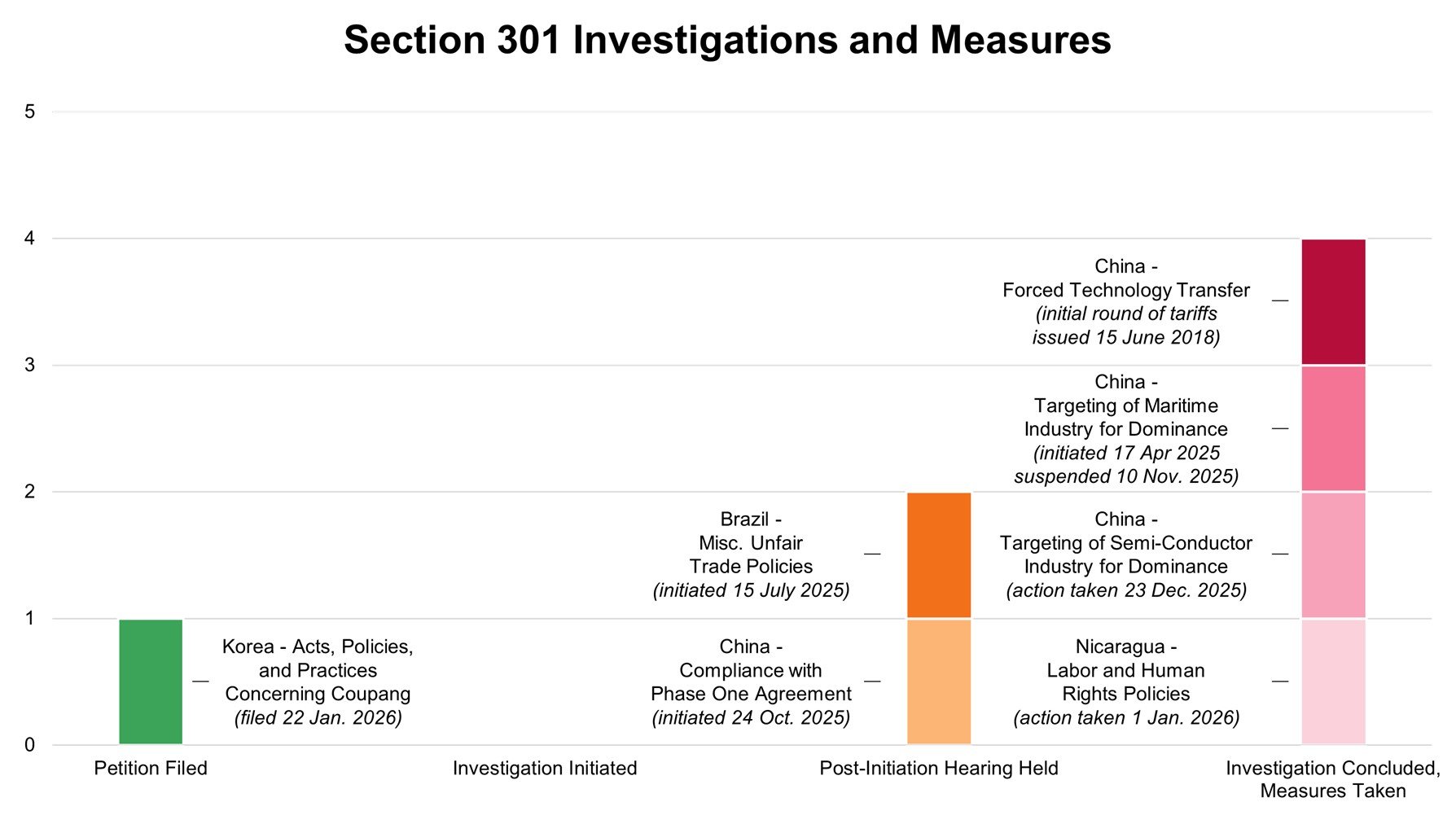

In 2018, the first Trump administration opened a Section 301 investigation into “China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation” and ultimately imposed tariffs on ~$200 billion worth of Chinese imports. These tariffs were renewed and expanded by the Biden administration and maintained under the current Trump administration (though diplomatic accords between the United States and China have led to the exclusion of certain products from the tariff regime). In addition, just this year, the second Trump administration has initiated several new Section 301 investigations against China and other nations, as shown in Figure 2 below. After the Supreme Court’s Learning Resources decision, the Trump administration also announced its intent to, “on an accelerated timeline,” initiate several new Section 301 investigations, including over “industrial excess capacity, forced labor, pharmaceutical pricing practices, discrimination against U.S. technology companies and digital goods and services, digital services taxes, ocean pollution, and practices related to the trade in seafood, rice, and other products.”

Figure 2 - Current Section 301 Investigations and Tariffs.

Other Potential Tariff Authorities

- Section 201 of the Trade Act of 1974. Permits the President to “take all appropriate and feasible action”—including imposing tariffs—when the International Trade Commission (the “ITC”) determines, after an investigation, that an import is or threatens to be “a substantial cause of serious injury” to a domestic industry that produces competing products. 19 U.S. Code § 2251. Section 201 tariffs cannot be imposed for longer than four years (extendable to eight) and are capped at 50% ad valorem. Section 201 has been invoked over 70 times since it was enacted in 1974, and U.S. courts have upheld the President’s broad power to implement Section 201 tariffs, emphasizing that judicial review is “very limited” and that relief is warranted only where the President or the ITC has committed a “clear misconstruction” of the statute.

- Antidumping and Countervailing Duty Laws Under the Tariff Act of 1930. Authorize the International Trade Administration (the “ITA”) and the ITC—after an investigation—to impose, and CBP to enforce, duties on imported goods sold at “less than fair value” that materially injure or threaten a domestic industry and to offset foreign subsidies that materially injure domestic industries. 19 U.S.C. §§ 1671–1677. AD/CVD duties are the most widely used U.S. trade measures, with 82 ongoing investigations and 817 AD/CVD orders as of February 24, 2026, across multiple industries.

Courts have extended substantial deference to the decisions of the ITA and ITC, so long as they respect the relevant procedural prerequisites. AD/CVD-based tariffs may therefore provide the Trump administration with a legally sturdy basis to continue implementing duties and import quotas on specific products from specific countries. However, the duties ordered must be targeted to specific countries and suppliers, time-limited and subject to ongoing administrative review. And because AD/CVD measures require lengthy investigations and substantial evidentiary showings—and afford the President little unilateral discretion—they may be a less attractive basis.

- Section 338 of the Tariff Act of 1930. Authorizes the President to impose tariffs up to 50% on goods produced in, or imported on the vessels of, foreign countries that discriminate against U.S. commerce. 19 U.S. Code § 1338. Section 338, however, has not been a meaningful basis for trade action since the 1940s, and the Code of Federal Regulations contains no implementing regulations specifying investigative procedures. Given its lack of use, Section 338 has also seen little (if any) modern judicial testing.

That said, the Federal Circuit in V.O.S. Selections, Inc. v. Trump (Fed. Cir. 2025)—the appellate court decision in the case later consolidated with Learning Resources at the Supreme Court—cited to Section 338 as an example of a statute that expressly delegates tariff-imposition authority to the President and—unlike other frameworks—does not, on its face, make presidential action explicitly contingent on particular agency findings. Section 338 could thus be viewed as a potential novel statutory basis for broad, discretionary tariff measures if the Trump administration chose to invoke it.

Remaining IEEPA-Based Policy Tools

The question before the Supreme Court was limited to the President’s use of IEEPA to impose certain tariffs, and other uses of IEEPA’s authority were not challenged. This means that the various national and economic security measures adopted by numerous administrations under IEEPA, particularly related to the imposition of U.S. financial or trade sanctions, remain fully in effect and unchanged by Learning Resources.

That noted, the case does illustrate that the strong deference historically shown by U.S. courts to executive action taken under IEEPA has limits and that courts will substantively consider challenges to such presidential action, even in the face of particularly strong argument from a President that an action falls under his foreign affairs or national security powers.

What Companies Should Do Now: Practical Strategies for Managing the Shifting Tariff Landscape

The shock absorbers that helped contain tariff exposure to date are unlikely to be as durable in a post-IEEPA landscape. In 2025, many companies were able to mitigate losses by exploiting shipment lags and increasing inventory in anticipation of threatened tariffs to avoid immediate exposure, rerouting their supply chains, negotiating exemptions and compressing profit margins. But shipment lags are inherently temporary, and inventories that were built up ahead of tariff implementation have been or are being drawn down and will eventually normalize. Rerouting supply chains does not guarantee that the new supply chains will remain unaffected, given the volatility of U.S. tariff policy and potentially novel tariff bases. Supply chains will also have fewer remaining margins to absorb incremental costs without repricing. Product-, company- and country-specific exemptions are discretionary and subject to any shifts in the Trump administration’s policy priorities, which remain unpredictable.

For the foreseeable future, therefore, companies should treat tariffs as an operating condition and continue building sustainable compliance, contracting and supply-chain strategies accordingly.

First, companies should carefully audit their existing contracts for vulnerabilities and seek to negotiate any new contracts strategically. Carefully constructed contracts can help companies more efficiently allocate tariff costs and avoid disputes with counterparties. As we previously detailed, suppliers will likely seek to avoid fixed obligation provisions; tailor indemnity and pass-through provisions in their favor, write expansive force majeure provisions or consider substantial hardship provisions, limit liquidated damages clauses and include flexible contract termination and renegotiation provisions. Purchasers will likely advocate for the opposite kinds of provisions. Both should tailor dispute resolution provisions to provide for efficient, lower-cost alternative dispute resolution, such as mediation and expedited arbitration.

Second, companies should develop a durable tariff risk mitigation approach, including with respect to disputes risk. This means: (i) mapping supply chains to identify areas at high risk of tariff exposure, including contractual relationships at various stages of the supply chain, to determine resulting dispute risk; (ii) ensuring compliance with procedural requirements in indemnity, pass-through, termination and renegotiation clauses; (iii) understanding the procedural, durational and magnitude limits imposed on the Trump administration by the various laws providing potential future bases for tariffs to identify opportunities for legal challenge; and (iv) for investors or acquirors, conducting tariff-exposure diligence, including stress-testing target-company supply chains, customer and supplier contracts and pricing flexibility for tariff-driven cost shocks.

Third, companies should operationalize tariff compliance and readiness through enhanced planning and organization. This could include: (i) establishing a cross-functional “tariff response” working group (trade compliance, procurement, finance, legal and commercial teams) with clear escalation paths and decision points; (ii) building rapid-response protocols for repricing, customer communications and supplier renegotiations triggered by defined tariff events; and (iii) strengthening trade-compliance operations fundamentals—such as customs classification, valuation and country-of-origin substantiation—to reduce overpayment risk and preserve optionality to pursue refunds, exclusions or other relief as policy shifts.

In sum, despite the recent success of the IEEPA challenge, the Trump administration’s tariff regime will endure, and businesses must prepare to navigate the evolving landscape, seeking durable solutions in the face of volatility.

This publication is for general information purposes only. It is not intended to provide, nor is it to be used as, a substitute for legal advice. In some jurisdictions it may be considered attorney advertising.