Key Takeaways:

- London Bridge is a cornerstone initiative to facilitate investment at Lloyd’s, giving investors a speedier route into the market versus establishing a de novo syndicate or purchasing a Lloyd’s operation and providing insurers and underwriters access to third-party capital to back their underwriting plans.

- London Bridge stands as the true success story of the United Kingdom’s onshore ISPV regime, enabling insurers to raise third-party capital through Lloyd’s sidecar structures and other insurance-linked securities, including catastrophe bonds.

- The structure holds particular appeal for asset managers seeking access to Lloyd’s specialist insurance business alongside durable asset management arrangements. Lloyd’s built-in “reinsurance to close” mechanism also offers a ready liquidity solution—a key draw for investors.

From its origins in a 17th century coffee house to today, Lloyd’s of London (“Lloyd’s”), the 330-year old insurance marketplace, is no stranger to reinvention and innovation. From expanding beyond marine insurance to overhauling the way investors participate in syndicates, Lloyd’s remains relevant in the 21st century in no small part because of its ability to “flex” the way it operates. The benefits of this can be seen in its financial results—during H1 2025, the underlying combined ratio of the marketplace was 82.1% with gross written premiums of £32.5 billion.

The London Bridge structure—arguably the UK’s only really successful onshore insurance special purpose vehicle regime—follows this tradition of growth and modernization by providing an alternative and speedier route for investors to provide capital to insurance businesses and for insurers and underwriters to access third-party capital to back their underwriting plans without needing direct regulatory approval.

As sidecar structures become more prevalent throughout the global insurance industry, the ability of Lloyd’s to attract capital in a similar fashion has been particularly attractive to investors. For example, we have seen asset managers such as Blackstone, Oaktree and Ontario Teachers’ Pension Plan make use of the structure, alongside strategic players including AIG, Beazley and OAK Enterprise, to both gain exposure to insurance business and create new asset management partnerships with insurers. In 2025 alone, London Bridge raised $1 billion in new institutional capital to support the 2026 year of account.

In this article, we explain how London Bridge works in practice and why (re)insurers and investors are paying increasing attention to it.

How Does London Bridge Work?

Legal Structure

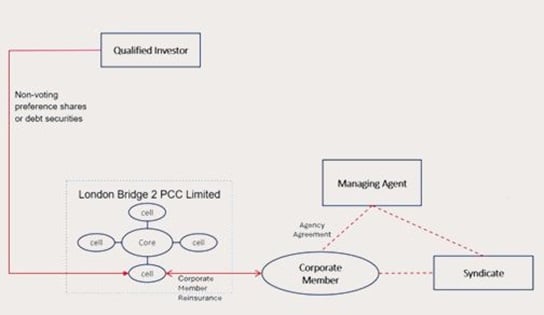

London Bridge itself takes the legal form of a UK-incorporated protected cell company. Each London Bridge cell supports a specific Lloyd’s syndicate and/or corporate member and is ring-fenced from every other cell and from the London Bridge core (which administers London Bridge as a whole). The assets held on behalf of a cell belong exclusively to that cell and may not be used to discharge liabilities incurred on behalf of or attributable to either the core or any other cell. Each cell’s transactions are entered into on a limited recourse basis and subject to priority of payments with investors’ rights subordinated to the reinsured corporate member or syndicate.

The investment, funneled through the London Bridge cell, provides the funds that a corporate member is required to deposit as Funds at Lloyd’s (“FAL”). In addition to these funds providing collateral to support the relevant syndicate’s underwriting at Lloyd’s, they will also cover the cell’s operating expenses. If additional FAL is required by the corporate member in respect of subsequent years of account or for cash calls issued by Lloyd’s from time to time, the investor may subscribe for further interests in the cell, usually subject to the terms of a reinsurance agreement between London Bridge (acting on behalf of the cell) and the corporate member or a framework agreement which outlines the relationship between the parties. The investor ultimately receives returns linked to the syndicate’s performance.

Transactions involving the London Bridge cell reinsuring the syndicate directly (rather than a corporate member) are generally structured as notes sold to institutional investors, the proceeds of which are used to collateralize reinsurance transactions between the relevant cell and the syndicate. This structure is particularly used for catastrophe bonds.

At Lloyd’s, each syndicate is ran on a “year of account” basis meaning that it will only underwrite events in a specific calendar year. Typically, each syndicate’s year of account is kept open for three years, after which it is closed by reinsurance into the next year of account of the syndicate (known as “RITC”). This later year takes over all liabilities and related claims handling costs of the closing year of account in return for a premium. Occasionally, a year of account may be reinsured by a different syndicate. While this means that the ultimate outcome on a particular year of account, backed by the FAL from the relevant London Bridge cell, cannot be determined with certainty until after the year of account has been reinsured to close, this procedure does ultimately provide a clear exit mechanic for potential investors.

Below is an abbreviated chart outlining a basic side-car style investment using the London Bridge structure and reinsuring the corporate member rather than the syndicate directly.

Regulatory Permissions

London Bridge is authorized by the UK Prudential Regulation Authority (the “PRA”) and Financial Conduct Authority (the “FCA”) as a multi-arrangement insurance special purpose vehicle. It is also licensed by Lloyd’s to reinsure business written at Lloyd’s and to issue securities (whether debt or equity) to raise the capital to fully fund those transactions. London Bridge’s regulatory permissions enable it to offer a range of risk transfer options to both corporate members and syndicates.

London Bridge has the authority to enter into transactions without further regulatory approval (provided the transaction documents contain certain mandatory terms), which has significantly reduced the amount of time required for investors to provide capital to support a Lloyd’s syndicate (compared with the time required to establish a de novo syndicate or corporate member).

The London Bridge Business Case

Access to Capital

The Lloyd’s / London Bridge structure has proved popular with insurers and underwriters looking for third party capital to support their underwriting plans and with investors looking for exposure to insurance business as an uncorrelated asset class, or where partnering with an insurer both to invest and manage the assets backing the insurance liabilities. The structure is also attractive for underwriting units or managing general agents (“MGAs”) looking for an alternative to traditional insurance companies to back their underwriting. For example, last year, Fidelis launched syndicate 2126, funded by Blackstone via the London Bridge platform, providing Fidelis with a further alternative source of capital to fund its underwriting expansion.

Exposure to Specialist Lines

Lloyd’s offers a highly concentrated market for coveted specialist insurance businesses. Investor appetite in this area is strong because of high growth opportunities, particularly in digital or other emerging risks. London Bridge allows investors to gain exposure to these specialty underwriting businesses without requiring a corporate member or syndicate to be established de novo (or acquired through a lengthy M&A process) at Lloyd’s.

Management of Insurance Assets

London Bridge serves as a key convergence point between asset management and insurance by providing an additional way for asset managers to access the insurance market and manage the assets backing a syndicate. In a first-of-its-kind transaction, the launch of syndicate 2478, a reinsurance syndicate, which is a multi-year participant on AIG’s outwards reinsurance program, supported by third-party capital from Blackstone, also utilized the London Bridge structure. This arrangement allows Blackstone to benefit from AIG’s strong underwriting performance and expertise across its diversified global property and casualty business and the opportunity to manage the syndicate’s assets.

Transfer of Specific Risks

London Bridge is an efficient way for insurers to transfer specific risks to the capital markets and raise capital. In 2024, Beazley issued the first excess of loss catastrophe bond via London Bridge, providing $100 million of multi-year indemnity reinsurance protection for named storm and earthquakes in the U.S., Canada and parts of the Caribbean across multiple Beazley underwriting entities. As testament to the effectiveness of London Bridge, in December 2025, Beazley successfully raised its third London Bridge natural catastrophe bond. Lloyd’s has previously stated that it hopes the London Bridge structure will also be used for non-property catastrophe bonds (particularly with a short or medium tail risks), which would be a distinguishing feature to other markets, particularly Bermuda, which have, to date, focused on property catastrophe bonds.

Reinsurance to Close

The RITC framework is part of the “business as usual” operations at Lloyd’s and provides an established liquidity mechanic for investors on the third anniversary of the relevant year of account. The calculation of the premium payable during the RITC process is overseen by an independent party, giving further comfort to investors.

Capital Efficiency

Capital provided at Lloyd’s to support members’ underwriting is available across multiple years of account (as part of the standard Lloyd’s operations). This is generally a distinguishing feature from other onshore or offshore side car arrangements.

Lloyd’s Rating and Chain of Security

Lloyd’s strength and robust capitalization are reflected in its financial ratings—Lloyd’s is currently rated A+ (AM Best) and AA- (Fitch and S&P). Much of this is drawn from the unique chain of security at Lloyd’s, which ultimately backs all insurance policies written at Lloyd’s and underpins the global license network. The chain of security has three key elements: (1) the syndicate’s assets (that is, the premiums received by the syndicate that are held in trust by the managing agent), (2) the FAL deposited by the underwriting members and (3) Lloyd’s central assets, including the Central Funds. Compared with other side car structures, policyholders and cedants reinsuring through a Lloyd’s/London Bridge structure can benefit from these protections.

Regulatory Advantages

London Bridge’s unique strength is that it has existing regulatory permissions from the PRA and FCA, as well as Lloyd’s. In practice, this means the regulators only need to be notified of a new transaction (that is, when a new cell is created or risk is assumed on behalf of a cell), which facilitates speed and ease of execution, and whilst investors will need to complete Lloyd’s AML checks, they will not need to be approved as controllers as they would if investing into a Lloyd’s managing agent or an authorized insurance company.

Tax Advantages

From a tax perspective, investing through London Bridge is advantageous because it falls within the scope of the UK Risk Transformation (Tax) Regulations 2017, which is a bespoke tax regime designed to attract insurance risk transformation business to the UK. As long as certain conditions are met, the London Bridge vehicle will be exempt from UK corporation tax and distributions made to investors will be exempt from withholding tax.

This publication is for general information purposes only. It is not intended to provide, nor is it to be used as, a substitute for legal advice. In some jurisdictions it may be considered attorney advertising.