SEC Exemptive Order Expands the Five-Business-Day Framework for Debt Tender and Exchange Offers

On June 30, 2026, the SEC Division of Corporation Finance issued an exemptive order (the “Order”) permitting qualifying tender and exchange offers for non-convertible debt securities to remain open for five business days rather than the 20 business days generally required by Rule 14e-1(a) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Order supersedes the SEC staff’s 2015 no-action letter and expands the abbreviated framework for debt transactions through formal exemptive relief from Exchange Act Rules 14e-1(a) and 14e-1(b). To use the Order, an offer must satisfy the following conditions:

- Eligible offeror and securities. The offer must be made by the issuer, a direct or indirect wholly owned subsidiary of the issuer or a parent company that directly or indirectly owns 100% of the issuer and must be made for a class or series of non-convertible debt securities, regardless of rating.

- Consideration. The offer may be made for cash and/or Qualified Debt Securities.[1]

- Partial offers. The Order permits offers for less than all of the outstanding class or series. If a partial offer is oversubscribed, securities must be taken up and paid for as nearly as may be pro rata and the offeror must use commercially reasonable efforts to announce the proration factor by 10:00 a.m. Eastern Time on the next business day after expiration, or as soon as practicable.

- Exchange offers. If Qualified Debt Securities are offered, the offer must be limited to qualified institutional buyers, non-U.S. persons and/or institutions that are accredited investors within the meaning of Rule 163B(c)(2)[2], in a transaction exempt from registration under the Securities Act of 1933, as amended.

- Consent solicitations. The offer may not be made in connection with a consent solicitation to amend the indenture or similar agreement governing the subject non-convertible debt securities where such amendment requires the consent of holders of more than a simple majority of the outstanding principal amount of the subject securities.

- Launch and dissemination. The offer must be announced by a widely disseminated press release by 10:00 a.m. Eastern Time on the commencement date. The release must include the basic terms of the offer, any proration procedures and an active hyperlink to the offer materials.

- Material changes. Any change in the percentage of securities sought, other than an additional two percent of the subject securities, or in the consideration offered must be widely disseminated by 9:00 a.m. Eastern Time on the third business day before expiration. Other material changes must be widely disseminated by 9:00 a.m. Eastern Time on the second business day before expiration.

- Withdrawal rights and payment. The offer must provide withdrawal rights at least until the earlier of expiration and, if the offer is extended, the tenth business day after commencement and at any time after the 60th business day after commencement if the offer has not been consummated. Consideration may not be paid until promptly after expiration under Rule 14e-1(c).

- Distressed and extraordinary transactions. The offer may not be made when a default or event of default exists under the relevant indenture or any other indenture or material credit agreement, or when the issuer is the subject of bankruptcy or insolvency proceedings, or has commenced a solicitation of consents for a “pre-packaged” bankruptcy proceeding, or if the board of directors of the issuer has authorized discussions with the issuer’s creditors to effect a consensual restructuring of the issuer’s outstanding indebtedness (“Distressed Scenarios”). The Order also limits use of the framework around change-of-control and other extraordinary transactions, competing tender offers and certain concurrent issuer tender offers.

The Order represents a meaningful modernization of the abbreviated debt tender and exchange offer framework. By replacing the prior no-action framework with exemptive relief and expanding the transactions eligible for a five-business-day offer period, the Order provides issuers with greater flexibility in structuring liability management transactions while preserving key investor-protection safeguards. As a result, the Order should facilitate the use of abbreviated debt tender and exchange offers in a broader range of ordinary-course refinancing and liability management transactions.

For more information, see Debevoise Update and the Exemptive Order.

[1] “Qualified Debt Securities” means non-convertible debt securities that are substantially similar in all material respects (including but not limited to the issuer(s), guarantor(s), collateral, lien priority, covenants and other terms) to either (1) the debt securities that are the subject of the tender offer or (2) the most recent issuance of debt securities that are pari passu to the debt securities that are the subject of the tender offer, except in either case for the maturity date, interest payment and record dates, redemption provisions and interest rate; provided that Qualified Debt Securities must have all interest payable only in cash.

[2] Institutional accredited investors covered include certain regulated financial institutions and investment vehicles, employee benefit plans, private business development companies, tax-exempt organizations, corporations, limited liability companies and other business entities meeting applicable asset or investment thresholds, as well as certain trusts, family offices and institutional family clients.

SEC Publishes Updated Regulatory Flexibility Agenda

On July 3, 2026, OIRA released its 2026 Regulatory Plan, including the SEC’s updated Regulatory Flexibility Agenda and Statement of Regulatory Priorities, which identify crypto assets, capital formation and retail access to private markets as key priorities.

Consistent with the themes of the SEC’s previous rulemaking agenda released in September 2025, the updated agenda reflects Chair Paul Atkins’s focus on deregulation, reducing compliance burdens and modernizing the federal securities laws. Rather than introducing new disclosure obligations, the agenda prioritizes revisiting existing rules that the SEC views as imposing unnecessary costs or impeding access to capital.

Among the most notable initiatives are proposals to streamline the registered offering process, revisit the accelerated filer framework, modernize the shareholder proposal process and replace mandatory quarterly reporting with an elective semiannual reporting regime. The agenda also contemplates continued work on developing a regulatory framework for crypto assets, modernizing the proxy solicitation process and rescinding the climate-related disclosure rules.

Although many of the listed items remain at the proposal stage and their timing remains uncertain, the agenda provides issuers, investment advisers and other market participants with a useful roadmap of the SEC’s expected areas of focus through Fall 2026 and beyond.

For more information, see Chair Atkins’s

statement on the 2026 Regulatory Agenda, the SEC

Statement of Regulatory Priorities and the

2026 Agenda.

CARB to Delay Implementation of SB 253

On June 24, 2026, CARB announced that it intends to revise its pending regulations implementing California’s Corporate Greenhouse Gas Reporting Program under the Climate Corporate Data Accountability Act (SB 253, codified in Health and Safety Code § 38532). Most notably, CARB stated that it will propose to defer the initial reporting deadline for Scope 1 and Scope 2 greenhouse gas (“GHG”) emissions disclosures from August 10, 2026 to November 10, 2026.

CARB also indicated that it intends to make limited revisions to the regulations to clarify certain reporting requirements and will release those proposed changes as part of a forthcoming 15‑day public comment period before resubmitting the rulemaking package to California’s Office of Administrative Law (“OAL”).

SB 253 was enacted in October 2023 and requires companies with more than $1 billion in revenue that do business in California to report Scopes 1 and 2 GHG emissions annually beginning in 2026 for the 2025 fiscal year, and Scope 3 GHG emissions beginning in 2027 for the 2026 fiscal year.

In February 2026, CARB approved an initial regulatory package implementing the program and submitted it to OAL for final review and approval. CARB has now withdrawn that submission to allow additional time to make limited revisions and clarifications to the regulations before re-submitting the package to OAL.

For more information, see

Debevoise Debrief and CARB’s

Notice of Upcoming Rulemaking. See also

Debevoise Debrief on the preliminary list of SB 253 covered entities and

Debevoise Debrief on the draft SB 253 reporting template. For more on California’s Climate Disclosure Laws, see

Debevoise Update and

Debevoise Debrief on the August 2025 CARB workshop.

Tokenized Stocks Debut Under Two Distinct Legal Frameworks

On July 2, 2026, Ondo Finance and Securitize took two distinct approaches to tokenized equity ownership, highlighting important differences in how blockchain-based equity products may be structured and what rights investors may receive. Ondo Finance created digital tokens on Ethereum that represent claims on existing shares of BlackRock’s iShares Core S&P 500 ETF and Micron Technology, while Securitize, on the same day that it began trading on the New York Stock Exchange (the “NYSE”), issued tokenized versions of its common stock to eligible U.S. investors on the Solana and Avalanche blockchains.

The two approaches reflect distinct legal ownership frameworks. Ondo’s tokens are structured as UCC Article 8 entitlements, rather than as ownership of the underlying securities themselves, meaning investors’ rights and remedies are tied to the intermediary. By contrast, Securitize’s tokens represent NYSE-listed common shares of Securitize, such that holders own the underlying shares and receive the corresponding shareholder rights.

The approaches also illustrate the different tokenization models described by the January 2026 joint staff statement from the SEC Divisions of Corporation Finance, Investment Management and Trading and Markets, which distinguished between issuer-sponsored tokenized securities and third-party tokenized securities. According to Ondo, its structure represents the first live implementation of the SEC staff’s third-party custodial tokenization model, under which blockchain tokens represent securities entitlements backed by underlying securities held by an intermediary. Securitize’s approach is consistent with the SEC staff’s issuer-sponsored tokenization model, under which the issuer tokenizes its own securities while preserving the rights associated with direct share ownership.

Together, the launches underscore that “tokenized stock” can describe materially different products. For investors and market participants, the key questions are not merely whether an equity interest is recorded on a blockchain, but whether the token represents the underlying security itself or a securities entitlement, what rights attach to the token, which intermediaries or custodians stand between the investor and the issuer and how existing securities-law frameworks apply to the product.

SEC Wins at the Supreme Court: SEC Disgorgement Doesn’t Require Pecuniary Harm

On June 4, 2026, the U.S. Supreme Court unanimously affirmed the Ninth Circuit’s decision in Sripetch v. SEC, holding that the SEC may obtain disgorgement of a defendant’s ill-gotten gains without proving that victims of the defendant’s securities law violation suffered pecuniary loss. The decision resolves a circuit split regarding the scope of the SEC’s disgorgement authority following the Supreme Court’s 2020 decision in Liu v. SEC and represents a significant victory for the SEC in preserving disgorgement as a central enforcement remedy.

Disgorgement has been part of the SEC’s enforcement toolkit since the 1970s. For decades, the SEC obtained disgorgement of gains wrongfully obtained through securities law violations, even where there was no discernible victim entitled to compensation. In Liu, the Supreme Court held that disgorgement is permissible equitable relief under the Exchange Act, where it does not exceed a wrongdoer’s net profits and is “awarded for victims.”

Shortly after Liu, Congress codified the courts’ authority to order disgorgement in SEC enforcement actions. However, since Liu, courts have divided over whether disgorgement requires proof that investors or other victims suffered pecuniary harm.

In Sripetch, the defendant had consented to a district court order finding that he engaged in fraudulent schemes involving numerous penny-stock companies and, together with associates, obtained more than $6.6 million in illicit proceeds. The SEC sought over $4.1 million in disgorgement as the net proceeds of the fraud. Sripetch objected, arguing that the SEC had not identified victims who suffered financial losses and therefore could not obtain disgorgement under Liu. The Ninth Circuit rejected that argument, and the Supreme Court affirmed.

The Supreme Court distinguished disgorgement from damages and held that proof of investor financial loss is not a prerequisite to disgorgement. Damages are measured by the plaintiff’s loss and are designed to make the plaintiff whole, while disgorgement is an equitable remedy measured by the defendant’s wrongful gain. Accordingly, the Court held that an individual may be a victim for purposes of disgorgement where the defendant invades the individual’s legally protected interests, even absent proof of financial loss.

The decision strengthens the SEC’s ability to seek disgorgement by barring challenges based solely on the absence of investor losses. However, the Supreme Court did not resolve whether the post-Liu amendments to the Exchange Act permit disgorgement where funds are not distributed to investors. Justice Thomas also issued a concurrence suggesting that future challenges may focus on whether defendants facing disgorgement are entitled to a jury trial. As a result, while Sripetch is an important win for the SEC, important questions regarding the scope and constitutional status of disgorgement remain unresolved.

For more information, see

Debevoise In Depth.

The Supreme Court Clarifies the Scope of Section 47(b): What’s Next for Listed Funds

On June 11, 2026, the U.S. Supreme Court held in FS Credit Opportunities Corp. v. Saba Capital Master Fund, Ltd. that Section 47(b) of the Investment Company Act of 1940 does not create an implied private right of action for rescission of contracts that allegedly violate the 1940 Act. The decision resolves a circuit split and narrows a potential path for private securities litigation under the 1940 Act, confirming that Section 47(b) is a remedial provision rather than an independent cause of action.

The case arose from activist challenges to listed closed-end funds that had opted into Maryland’s Control Share Acquisition Act, which is intended to limit voting rights associated with shares acquired above specified ownership thresholds unless other shareholders approve those voting rights. Saba Capital argued that the funds’ use of the statute conflicted with Section 18(i) of the 1940 Act, which generally requires that each share of stock issued by a registered management investment company have equal voting rights, and that Section 47(b) allowed Saba to seek rescission or related relief.

The Supreme Court rejected that theory, concluding that Section 47(b) describes remedies that may be available once a party is properly before the court, but does not itself authorize private parties to sue. The Court also emphasized that Congress created express private rights of action elsewhere in the 1940 Act and provided the SEC with substantial enforcement authority, which weighed against implying a broader private enforcement mechanism under Section 47(b).

For listed closed-end funds and business development companies, the ruling provides additional flexibility, but not a free pass. It may be particularly important for those facing activist campaigns, as it limits the pathways for challenging control-share provisions, defensive bylaws and other governance protections. However, the decision does not resolve the substantive legality of control-share provisions or other defensive tools under the federal securities laws.

The decision also arrives as the SEC considers broader modernization proposals affecting public-company reporting, registered offerings and listed funds. The SEC’s May 19, 2026 rulemaking packages would expand offering flexibility for listed business development companies and registered closed-end funds, simplify filer status under the Exchange Act for many reporting companies and extend certain scaled disclosure accommodations to a broader set of issuers. Together with the Supreme Court’s decision, those proposals may create an opportunity to reassess the listed fund structure, including governance tools, proxy and shareholder mechanics, communications flexibility, secondary-market price formation and regulatory accommodations for listed closed-end funds and business development companies.

For more information, see

Debevoise In Depth.

SEC Publishes Draft Strategic Plan for Public Comment

On June 2, 2026, the SEC published its Draft Strategic Plan for public comment. The draft plan identifies three strategic goals for the agency:

- renewing the SEC’s regulatory policy focus to promote innovation, capital formation, market efficiency and investor protection;

- enhancing regulatory practices by increasing stakeholder engagement and compliance efforts while returning enforcement to policing violations of established law; and

- optimizing the agency’s operational efficiency through organizational, technology and performance-management reforms.

The draft plan describes a policy agenda focused on facilitating capital formation and market participation, including by supporting innovation in financial markets and modernizing disclosure, registration and market-structure requirements. It also emphasizes the SEC’s intent to engage more actively with market participants and other stakeholders, to make greater use of economic analysis and to reassess existing rules and practices where they may be outdated, duplicative or unnecessarily burdensome.

With respect to enforcement, the draft plan states that the SEC will seek to focus on violations of established law and return to predictable, transparent enforcement grounded in statutory authority. The plan also highlights efforts to improve the SEC’s internal operations, including through technology modernization, data-management improvements, workforce planning and enhanced performance measurement.

For more information, see the

Draft Strategic Plan.

Board Refreshment: More than a Compliance Exercise

As companies face increasingly complex strategic, operational and regulatory challenges, boards should regularly evaluate whether they have the right mix of skills, experience and perspectives to provide effective oversight. Building a board refreshment strategy requires boards, nominating and governance committees and management teams to consider the following key factors as they evaluate board composition and long-term succession.

- Start with Succession Planning. Boards should establish an ongoing process for evaluating future leadership needs and preparing for expected and unexpected director departures, rather than reacting only when vacancies arise.

- Use Board Evaluations to Inform Refreshment Decisions. Effective evaluations can help boards assess whether board and committee composition meet current and future needs, identify expertise gaps and determine whether director succession should become a near-term priority.

- Periodically Assess Board Composition. Boards should periodically consider whether their overall composition remains aligned with the company’s strategic priorities and risk profile, including by evaluating industry knowledge, financial and operational expertise, leadership experience, tenure, age and diversity of backgrounds and perspectives.

- Maintain a Pipeline of Director Candidates. An active candidate pipeline can help boards respond quickly to unexpected departures and recruit directors whose backgrounds align with the company’s long-term strategic objectives.

Boards that approach refreshment as an ongoing strategic priority—rather than simply a compliance exercise—will be better positioned to maintain the expertise, independence, and diversity of perspectives necessary to provide effective oversight in an increasingly dynamic business environment. Succession planning, board evaluations, periodic assessments of board composition and thoughtful recruitment are all important components of that process.

For more information, see

Debevoise Debrief.

SEC Rulemaking Agenda

The SEC’s 2026 Regulatory Agenda was posted in July 2026. A summary of pending rule changes is included below, along with the SEC’s announced release date. For more information, see the full regulatory agenda here.

|

Title

|

Stage of Rulemaking

|

Latest Action

|

|

Asset-Backed Securities Registration and Disclosure Enhancements

|

Prerule Stage

|

Rule Proposal Expected October 2026

|

|

Evaluating the Consolidated Audit Trail

|

Prerule Stage

|

Proposed April 2026

|

|

Rule 144 Safe Harbor

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Foreign Private Issuer Eligibility Enhancements

|

Proposed Rule Stage

|

|

Crypto Assets[3]

|

Proposed Rule Stage

|

Rule Proposal Expected July 2026

|

|

Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies

|

Proposed Rule Stage

|

Proposed May 2026

|

|

Registered Offerings Reform

|

Proposed Rule Stage

|

|

Updating the Exempt Offering Pathways

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Rationalization of Disclosure Practices

|

Proposed Rule Stage

|

|

Shareholder Proposal Modernization

|

Proposed Rule Stage

|

|

Semiannual Reporting

|

Proposed Rule Stage

|

Proposed May 2026

|

|

Executive Compensation Disclosure Reform

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Financial Institution Resolution Transactions

|

Proposed Rule Stage

|

|

Amendments to Certain Proxy Rules

|

Proposed Rule Stage

|

|

Rescission of Climate-Related Disclosure Rules

|

Proposed Rule Stage

|

Proposed June 2026

|

|

Updates to “Small Entity” Definitions for Purposes of the Regulatory Flexibility Act

|

Proposed Rule Stage

|

Proposed January 2026

|

|

Amendments to Form N-PORT

|

Proposed Rule Stage

|

Proposed February 2026

|

|

Amendments to Rule 17a-7 Under the Investment Company Act

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Amendments to the Custody Rules

|

Proposed Rule Stage

|

|

Electronic Delivery of Information Under the Federal Securities Laws[4]

|

Proposed Rule Stage

|

|

Enhancing Retail Exposure to Private Markets

|

Proposed Rule Stage

|

|

Affiliated Securities Lending Agent Arrangements

|

Proposed Rule Stage

|

|

Form PF; Reporting Requirements for All Filers and Large Hedge Fund Advisers

|

Proposed Rule Stage

|

Proposed April 2026

|

|

Pay-to-Play Reform

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Amendments to Investment Adviser Recordkeeping Rule

|

Proposed Rule Stage

|

|

Transfer Agents

|

Proposed Rule Stage

|

|

Publication or Submission of Quotations Without Specified Information

|

Proposed Rule Stage

|

Proposed March 2026

|

|

Amendments to Broker-Dealer Financial Responsibility and Recordkeeping and Reporting Rules Regarding Crypto Assets

|

Proposed Rule Stage

|

Rule Proposal Expected July 2026

|

|

Crypto Market Structure Amendments

|

Proposed Rule Stage

|

|

Amendments to the Trade-Through Rule

|

Proposed Rule Stage

|

Proposed June 2026

|

|

Definition of Dealer

|

Proposed Rule Stage

|

Rule Proposal Expected October 2026

|

|

Enhanced Oversight for U.S. Government Securities Traded on Alternative Trading Systems

|

Proposed Rule Stage

|

|

Amendments to Rule 17Ab2-1 and Form CA-1

|

Proposed Rule Stage

|

|

Amendments to Rule 17Ad-22(e)(18) and 15c3-3

|

Proposed Rule Stage

|

|

Regulatory Status of Finders

|

Proposed Rule Stage

|

|

Rule 17a-4 “Business as Such” Clarification

|

Proposed Rule Stage

|

|

Amendments to Rule 13f-2, Related Form SHO, and Regulation SHO

|

Proposed Rule Stage

|

|

Amendments to Rule 10c-1a

|

Proposed Rule Stage

|

[3] Submitted to the White House for OIRA review in March 2026.

[4] Submitted to the White House for OIRA review in June 2026.

Securities Law-Related Legislation

A summary of selected recent securities law-related legislation proposed in June 2026 follows:

|

Name of Bill

|

Description of Bill

|

Latest Action

|

|

H.R.9490

|

To defer part of the compensation of senior employees of large financial institutions and their subsidiaries, and to use such deferred amounts to pay any civil or criminal fines levied on the institution or subsidiary.

|

House - 06/25/2026 Referred to the House Committee on Financial Services.

|

|

H.R.9462

|

To amend the Exchange Act to prohibit mandatory pre-dispute arbitration agreements, and for other purposes.

|

House - 06/25/2026 Referred to the House Committee on Financial Services.

|

|

S.4937

|

A bill to amend the Exchange Act to prohibit mandatory pre-dispute arbitration agreements, and for other purposes.

|

Senate - 06/24/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

|

H.R.9434

|

A bill amending the federal securities laws to require rulemakings to consider the cumulative effects of the rule with certain other final and proposed rules.

|

House - 06/24/2026 Referred to the House Committee on Financial Services.

|

|

H.R.9329

|

A bill to restructure and reform the SEC by increasing regulatory accountability and congressional oversight, strengthening cybersecurity, streamlining public company audit oversight and modernizing the SEC’s rulemaking and enforcement processes.

|

House - 06/18/2026 Referred to the House Committee on Financial Services.

|

|

S.4743

|

A bill requiring the Office of Financial Research to collect and report data on financial institutions’ debt and equity exposure to AI-related companies and issue recommendations to mitigate financial stability risk.

|

Senate - 06/10/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

|

S.4690

|

A bill to amend the Securities Act of 1933 to expand the ability to use testing the waters and confidential draft registration submissions, and for other purposes.

|

Senate - 06/04/2026 Read twice and referred to the Committee on Banking, Housing, and Urban Affairs.

|

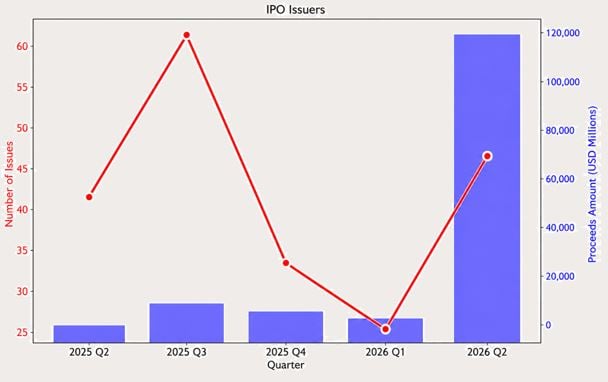

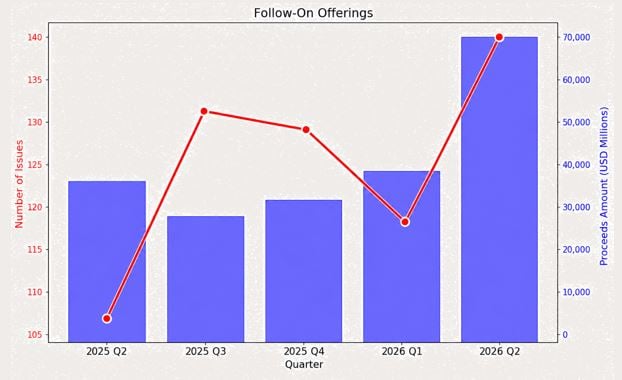

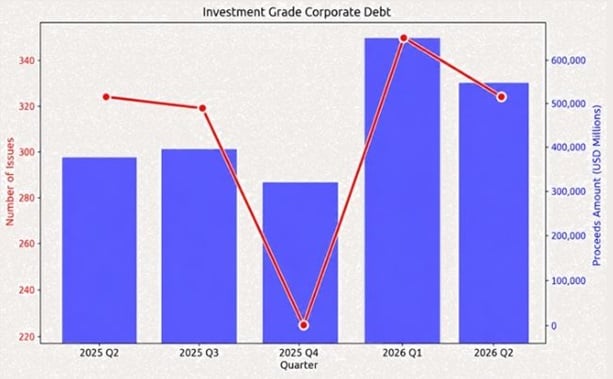

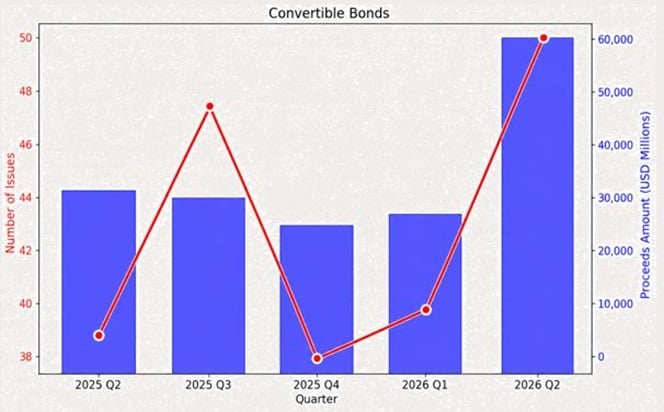

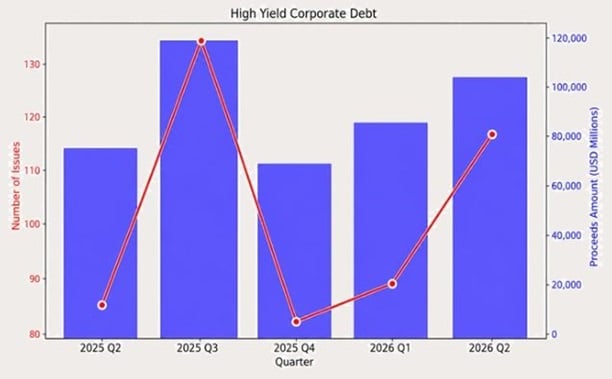

Markets At A Glance

The below market snapshot shows the volume of U.S. IPOs, follow-on offerings, investment grade corporate debt issuances, convertible bonds issuances and high-yield corporate debt issuances from the second quarter of 2025 through the second quarter of 2026.

This publication is for general information purposes only. It is not intended to provide, nor is it to be used as, a substitute for legal advice. In some jurisdictions it may be considered attorney advertising.